Apart from buying a home, superannuation is likely to be the biggest investment most Australians will make in their lifetime.

It’s also one of the most tax-effective ways to save for retirement. The Government provides tax concessions for superannuation, which include concessional taxation rates for certain contributions, as well as for earnings on investments.

Types of superannuation contributions

There are generally two types of superannuation contributions you can make to super.

Concessional contributions | Concessional contributions are generally made by your employer on your behalf, such as the super guarantee and salary sacrifice contributions, or are contributions that you make personally and claim as a tax deduction. An annual limit applies to the total amount of concessional contributions that can be made by your or on your behalf. This limit is known as the concessional contributions cap. |

Non-concessional contributions | Non-concessional contributions are generally contributions you make from your after-tax money, for example from the salary you’ve received from your employer, and for which you haven’t claimed a tax deduction. They can also be contributions that are made to your super by your spouse. These contributions are subject to an annual contribution limit, known as the non-concessional contributions cap, which is four times the concessional contributions cap. Your own cap might be different. For more information see the ATO website. |

Tax effectiveness of superannuation

Contributions

The tax arrangements applying to superannuation contributions broadly depend on the type of contributions made and whether the contribution is within the relevant contribution cap.

Concessional contributions are taxed at 15 per cent in the fund when they are made*. These tax rates are generally less than those that apply on income that is paid to you personally and taxed at individual marginal tax rates.

Non-concessional contributions on the other hand, are not taxable in the fund when they are made.

More information, including the current contribution caps and the treatment of contributions above the caps, can be found on the ATO website.

* An additional 15 per cent tax (known as Division 293 tax) may apply to concessional contributions if your income exceeds a certain threshold.

Tax within your fund

Within your superannuation account, investment income is typically taxed at a maximum rate of 15 per cent, which is generally less than individual marginal tax rates. Once you start a superannuation pension (excluding transition-to-retirement pensions), the investment earnings in your pension account are completely tax free.

Typically, the tax advantages of superannuation help your retirement savings grow faster than they would if held outside super.

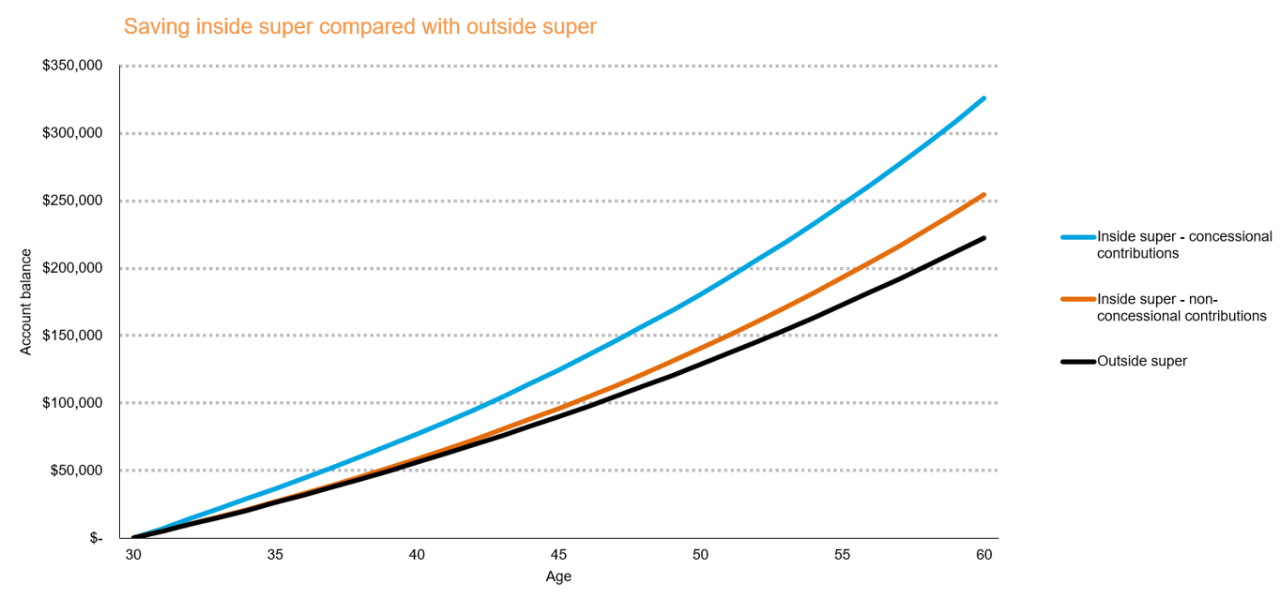

Example: Alice’s super savings

Alice is 30 years old and has $5,000 after tax available to save per year. She can choose to invest this inside or outside superannuation. She can also choose how she contributes this money into her superannuation to potentially increase her savings.

The chart below shows three options for Alice to save from age 30 to age 60.

The chart below shows the results of the following scenarios:

- If Alice contributes $5,000 per year into her superannuation account as a non-concessional contribution, she will have $254,770 at age 60.

- If Alice invests $5,000 per year outside superannuation, her investment will grow to $222,598 at age 60.

- If Alice salary sacrifices* the pre-tax equivalent of $5,000 into her superannuation account as a concessional contribution each year, her account balance will grow to $325,681 at age 60.

* Many employers offer salary sacrifice arrangements to their employees. Under these arrangements, employees have the option of forgoing some of their pre-tax salary in return for additional superannuation contributions.