Your integrated cash management solution

Discover how Fuse Wealth deliver more for their clients with integrated cash flow management.

Choose the smarter wealth ecosystem

that can help you deepen your client relationships and help your firm thrive.

A smarter wealth ecosystem

We’ve built a smarter product and technical ecosystem designed to integrate seamlessly with the business solutions you already rely on and delivering the efficiencies you need.

The best minds in Macquarie

You have our team behind you. We get to know you, then bring the best minds within Macquarie to help strengthen your business.

Wealth Matters

Insights, updates and resources to help you efficiently manage and grow your business.

Explore the wealth solutions ecosystem

A guide to active cash management

Actively avoid the risks of hidden, unproductive or idle cash.

Forms and tools

Access the tools and resources you need efficiently and seamlessly – forms, offer documents and performance reporting.

Macquarie building_ 1ES

Macquarie building_ 1ES

Macquarie Wrap helps you unlock opportunity other advisers can't

Discover new efficiencies with Macquarie's platform

Banking solutions

Successful scaling: insights from Alteris Financial Group

After completing eight acquisitions in eight years, we spoke to Alteris Financial Group about the tools, technology and principles they rely on to successfully scale.

Five red flags: How to help your clients avoid financial scams

More than 600,000 Australians reported a scam in 2023, collectively losing over $2.74 billion. Lured by too-good-to-be-true investment opportunities or under pressure from fake fraud report calls, high net worth advised clients are among the growing numbers of investors being hooked by scammers.

Watch video

Loading video...

Protect your firm: Business email compromise scams

Business email compromise is one of the leading causes of fraud-related financial loss in Australia. You and your team can’t afford to be complacent.

Watch video

Loading video...

Protect your firm: Impersonation scams

An impersonation scam is when a scammer impersonates a bank or other service company and contacts someone by phone or SMS, asking them to authorise transactions, make a payment or provide personal information.

Security and scams hub

Arm yourself with information on the latest scams and fraud activity. Learn how to protect yourself and share useful with your clients about how to stay safe online and beyond.

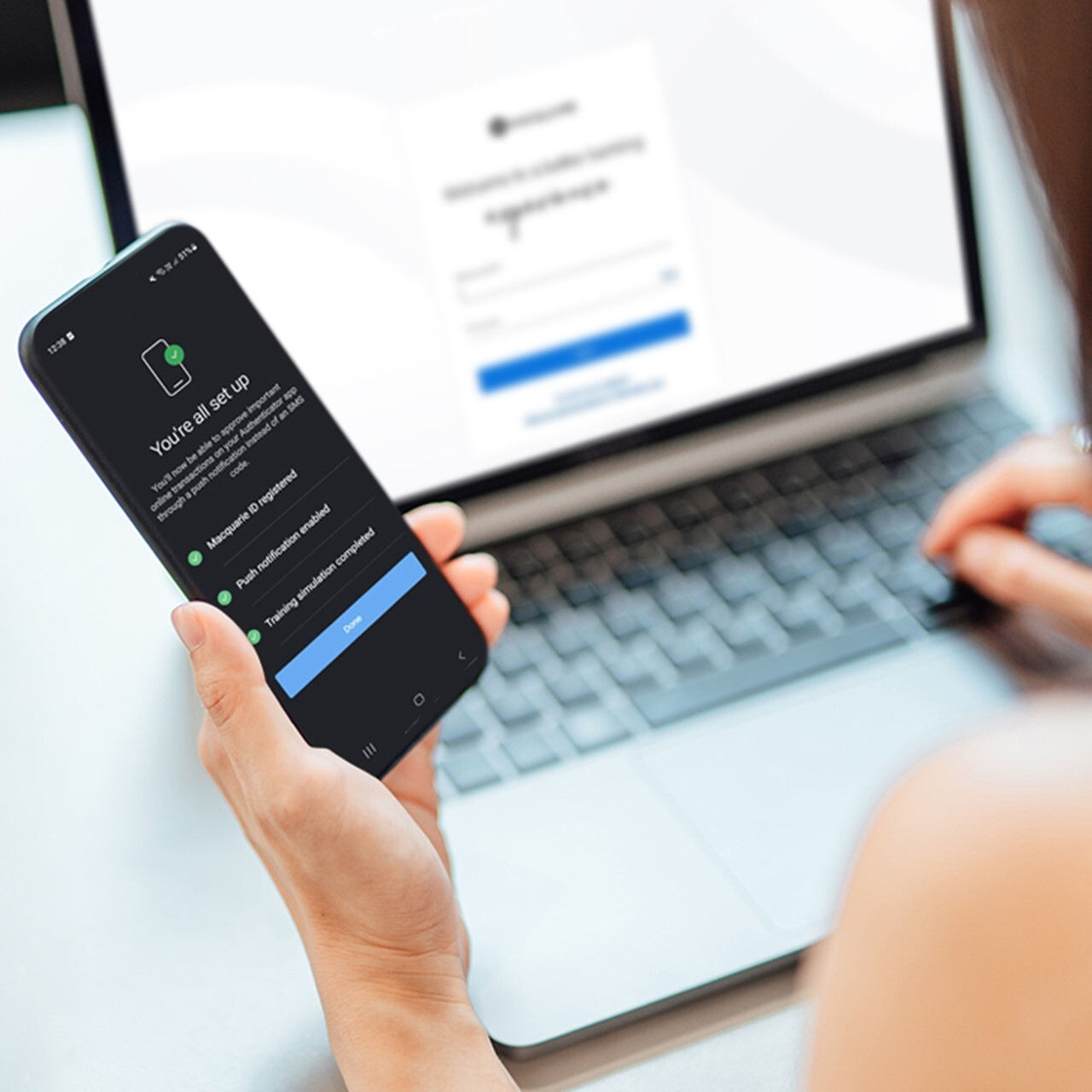

Macquarie Authenticator

Macquarie Authenticator is a secure digital verification and transaction approval tool.

Perspective on value creation

Building value through mergers and acquisitions

At face value, mergers and acquisitions are a fast and effective path to growth. But to execute one successfully, you need a proven strategy, careful and extensive planning, and a host of trusted advisers to guide the process. Read more about Macquarie’s proven framework for navigating an M&A deal.

Contact us

Need help? If you’re an adviser, please contact us via live chat in Adviser Online. If you’re a client, please call

More information on AML/CTF requirements

Additional information

Unless stated otherwise, this information has been prepared by Macquarie Bank Limited AFSL and Australian Credit Licence 237502. It is provided for the use of licensed and accredited brokers and financial advisers only. In no circumstances is it to be used by a potential client for the purposes of making a decision about a financial product or class of products.

This information doesn’t take into account your needs or financial situation - consider our Product Disclosure Statement (or other applicable offer document(s)) available on the Macquarie website, to decide if our products are right for you and whether you should acquire or continue to hold a product.

Target Market Determinations for Macquarie issued products are available at our Design and Distribution hub.

The Macquarie Cash Management Account, The Macquarie Cash Management Accelerator Account and Macquarie Bank Term Deposit are basic deposit products issued by Macquarie Bank.