A trust is a legal arrangement whereby a legal entity (a trustee, i.e. a company or individual(s)) holds an asset for the benefit of one or more beneficiaries.

- What's a trust?

- Does a trust deed need to be submitted?

- What types of trusts can apply for a home loan?

- What are the common parties in a trust arrangement?

- What roles in a trust can be a party or borrower of a home loan?

- What does a trust structure need to have to be acceptable for lending?

-

What are examples of acceptable and unacceptable trust structures?

- 1. Acceptable with individual trustee

- 2. Unacceptable with individual trustee - Third party Appointor

- 3. Acceptable with corporate trustee

- 4. Acceptable with corporate trustee - Complex structure

- 5. Unacceptable with corporate trustee - Third party Appointor

- 6. Unacceptable with corporate trustee - Complex structure

- 7. Unacceptable with corporate trustee - Not a natural person

- How do I input trust structures into ApplyOnline?

What's a trust?

Does a trust deed need to be submitted?

Where a trust is the borrower on a loan, we require a certified copy of the trust deed to be provided on submission. This is required to meet our obligations for Anti-Money Laundering and Counter Terrorism Financing (AML/CTF) Act 2006 (Cth).

A formal trust deed outlines how the trust operates, what powers the trust has, the beneficiaries that will receive distributions and legal responsibilities.

The trust deed must be:

- certified in the last 24 months, and

- certified using a wet-signature (i.e. printed and signed).

What types of trusts can apply for a home loan?

We’ll lend to both:

We don’t currently lend to hybrid trusts, or multiple trusts in one application.

Fixed trusts (including unit trusts)

In a fixed trust, beneficiaries are entitled to a predetermined and ‘fixed’ share in assets and income. This means the income distribution across beneficiaries is fixed and can’t vary.

A unit trust is a type of fixed trust where the share in the assets and income is represented by units. Unit holders of a unit trust must be individuals.

Discretionary family trusts

Discretionary family trusts provide the trustee with ‘discretion’ over who receives the distributions from the trust. The discretion must be exercised in accordance with the terms of the trust deed.

The trustee can use their discretion each year to decide which beneficiaries receive income, and how much. Therefore, the distribution each year can vary.

What are the common parties in a trust arrangement?

Common parties to a trust arrangement include the Settlor (or Trustor), the Trustee, the Appointor and the Beneficiary. The following table provides a short description of each role.

| Role | Who | What |

| Settlor or Trustor | Person | Creates the trust and transfers assets into it. They set the terms and conditions of the trust |

| Trustee | Person or entity | Responsible for managing the trust according to its terms and for the benefit of the beneficiaries (family trust) or unit holders (unit trust). |

| Beneficiary - unit trusts | Person or entity | Holds units in the trust and benefits from the trust's income and capital. They have a fixed entitlement to the trust’s income and capital based on number of units held. |

| Beneficiary - family trust | Person or entity | Benefits from the trust to the discretion of the Trustee for both income and capital. |

| Appointer/Controller - family trust | Person or entity | Has the power to appoint or remove trustees. |

What roles in a trust can be a party or borrower of a home loan?

For the purposes of lending to a trust entity, we consider both control and ownership of the trust. Therefore, we’ll only offer lending to trust structures where all beneficial owners and controllers (e.g. an Appointor/Controller) are a party to a loan. Where the controller (e.g. the Appointor) isn’t a party to the loan, we won’t consider lending to that structure.

Beneficial owners and controllers for the trust are individuals who (either indirectly or directly) control or own the trust. These aren’t necessarily the same as the beneficiaries.

Acceptable parties include:

- Appointor/Controller (also known as Protector/Nominator etc.)

- Individual trustees (e.g. Wendy Smith and John Smith as trustee for The Smith Family Trust)

- Corporate trustees (e.g. ABC Pty Ltd as trustee for The Smith Family Trust)

- Including the Trustee company’s directors and shareholders, who must also be natural persons.

Criteria for trust borrowers to meet

All trust borrowers must meet all the following criteria:

- Be a non-trading entity

- Own less than five properties

- Have turnover less than $75 million, and

- Have only natural persons as beneficiaries (e.g. Wendy Smith is acceptable, ABC Pty Ltd isn’t acceptable).

What does a trust structure need to have to be acceptable for lending?

The following requirements must be met for a trust structure to be considered acceptable:

- The trust Borrower must match the trust deed

- All trustees must be a party to the loan (typically can be confirmed from the front cover of the trust deed)

- If the Trust has a corporate trustee, then:

- all Shareholders must be natural persons and Directors

- all Directors must be a party to the loan and provide a guarantee

- all Shareholdings must be beneficially held, and

- no Shareholding to Bearer or Nominee share classes.

- The Appointor/Controller must be the same as the individual trustees or the Directors of the corporate trustee.

Where any of the requirements aren’t met, the trust structure would be considered unacceptable. There are no exceptions to the above requirements.

What are examples of acceptable and unacceptable trust structures?

Below are some examples of trust structures that are acceptable and unacceptable, depending on the type of trustee.

- Acceptable with individual trustee

- Unacceptable with individual trustee – Third party Appointor

- Acceptable with corporate trustee

- Acceptable with corporate trustee – Complex structure

- Unacceptable with corporate trustee – Third party Appointor

- Unacceptable with corporate trustee – Complex structure

- Unacceptable with corporate trustee – Not a natural person

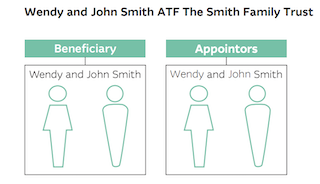

1. Acceptable with individual trustee

As all beneficial owners are a party to the loan, we can accept this trust structure.

Scenario: Wendy and John Smith as trustee for The Smith Family Trust

- Borrower: Wendy Smith and John Smith in their own right, and as trustee for The Smith Family Trust

- Beneficial Owner and Appointors: Wendy Smith and John Smith (as they’re both Trustees and both appointors).

The diagram below illustrates this scenario:

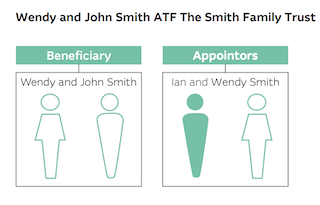

2. Unacceptable with individual trustee - Third party Appointor

As one of the Appointors (Ian Smith) is a third party, we can’t accept this trust structure.

Scenario: Wendy and John Smith as trustee for The Smith Family Trust

- Borrower: Wendy Smith and John Smith in their own right, and as trustee for The Smith Family Trust

- Beneficial Owner: Wendy and John Smith as trustees of the trust

- Appointors/Controller: Wendy Smith and Ian Smith.

The diagram below illustrates the scenario:

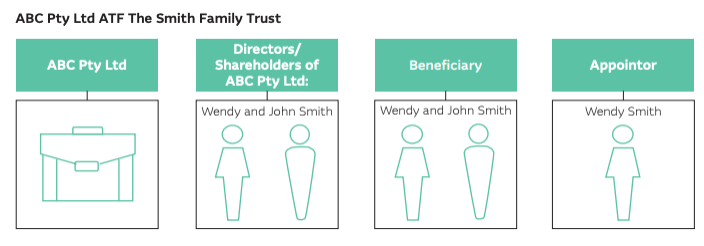

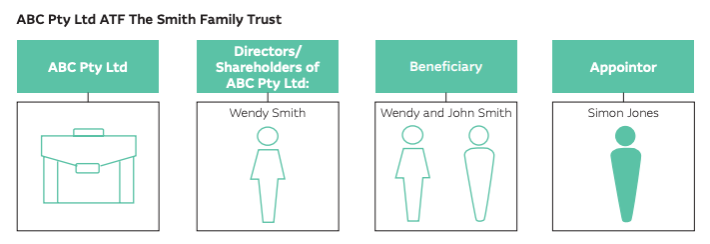

3. Acceptable with corporate trustee

As all beneficial owners (and appointors) are a party to the loan, we can accept this trust structure.

Scenario: ABC Pty Ltd as trustee for The Smith Family Trust

- Borrower: ABC Pty Ltd in its own right as trustee for The Smith Family Trust

- Guarantor: Wendy and John Smith as Director/Shareholders of the Trustee Company, therefore providing personal guarantees in their individual capacities

- Beneficial Owner: Wendy and John Smith are the Directors and Shareholders of the Trustee Company

- Appointor/Controller: Wendy Smith.

The diagram below illustrates this scenario:

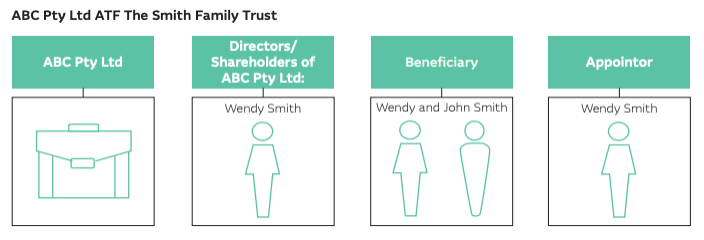

4. Acceptable with corporate trustee - Complex structure

We can accept this trust structure as there is a common natural person (i.e. Wendy Smith) as Director/Shareholder, Beneficiary and Appointer. There is also additional options to include John Smith as a guarantor, if required for servicing.

Scenario: ABC Pty Ltd as trustee for The Smith Family Trust

- Borrower: ABC Pty Ltd in its own right as trustee for The Smith Family Trust

- Guarantor: Wendy Smith as Director/Shareholder of the Trustee Company, therefore providing personal guarantee in her individual capacity

- Beneficial Owner: Only Wendy Smith as she is sole Director and Shareholder of the Trustee Company

- Appointor/Controller: Wendy Smith.

Key points in this scenario

- Wendy is the sole Director and Shareholder of ABC Pty Ltd. Therefore, we would take a guarantee from Wendy Smith, and

- John Smith shouldn’t be tied into the transaction. Except, if servicing isn’t evident with only Wendy’s income and the income generated by the Trust. If required, a guarantee from John Smith could be taken to support servicing, as he's a beneficiary of the Trust.

The diagram below illustrates this scenario:

5. Unacceptable with corporate trustee - Third party Appointor

This structure is unacceptable because the Appointor is a third party (i.e. Simon Jones).

Scenario: ABC Pty Ltd as trustee for The Smith Family Trust

- Borrower: ABC Pty Ltd as trustee for The Smith Family Trust

- Guarantor: Wendy Smith as she is a Director of the Trustee Company, therefore providing personal guarantee in her individual capacity

- Beneficial Owner: Wendy as sole Director and Shareholder of the Trustee Company

- Appointor/Controller: Simon Jones.

The diagram below illustrates this scenario:

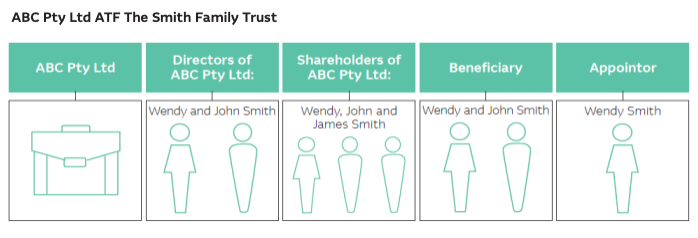

6. Unacceptable with corporate trustee - Complex structure

Third party shareholders who aren’t beneficiaries are unacceptable (e.g. James Smith).

Scenario: ABC Pty Ltd as trustee for The Smith Family Trust

- Borrower: ABC Pty Ltd as trustee for The Smith Family Trust

- Guarantor: Wendy Smith and John Smith as they are Directors of the Trustee Company, therefore they both provide personal guarantee in their individual capacities

- Beneficial Owner: Wendy Smith and John Smith as they are Directors and Shareholders as sole Director of the Trustee Company, AND James Smith as Shareholder of the Trustee Company

- Appointor/Controller: Wendy Smith.

This structure is unacceptable as not all beneficial owners of the corporate trustee are party to the loan.

- James Smith is a shareholder but not a Director of the corporate trustee, and

- he's also not a beneficiary of the trust, therefore can’t be added as a party to the loan.

The diagram below illustrates this scenario:

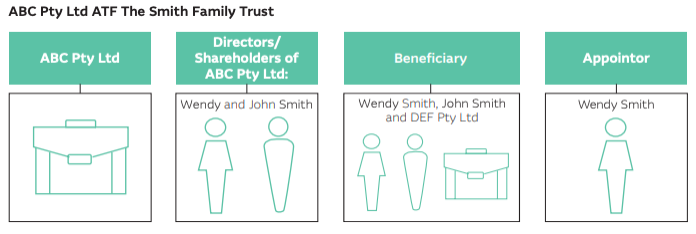

7. Unacceptable with corporate trustee - Not a natural person

This structure is unacceptable as one of the beneficiaries isn't a natural person, i.e DEF Pty Ltd. Therefore this structure isn’t an acceptable borrower/guarantor.

Scenario: ABC Pty Ltd as trustee for The Smith Family Trust

- Borrower: ABC Pty Ltd as trustee for The Smith Family Trust

- Guarantor: Wendy Smith and John Smith as they are Directors and Shareholders of the Trustee Company, therefore, they both provide personal guarantee in their individual capacities

- Beneficial Owner: Wendy Smith and John Smith as they are Directors and Shareholders as sole Director of the trustee company, and company DEF Pty Ltd (owned by John Smith)

- Appointor/Controller: Wendy Smith.

The diagram below illustrates this scenario:

How do I input trust structures into ApplyOnline?

To help you accurately submit a trust home loan application in ApplyOnline, we’ve created the following guides:

Related articles

-

Accessing our credit policy and calculators -

Submitting self-employed applications -

Understanding acceptable securities and maximum LVR

Search Help Centre

Log in to Broker Portal

Track your applications, view our processing times and easily access your existing customer's loan details, all within Macquarie Broker Portal.

Search Broker Help Centre

Find answers faster to your everyday queries with Broker Help Centre. Search by keywords or by category to find exactly what you need, when you need it.

Meet the team

Our BDM team provides you and your customers with world-class service and the support you need throughout the home loan journey. Get to know the BDMs in your state today.