Landmark rulings in 2020 and 2021 are prompting healthcare businesses to review how they run their practices. But what do these rulings mean, and how could they impact your business model?

These were the questions we explored at our webinar on the latest healthcare payroll tax rulings.

Accounting expert Heath Stewart, Head Partner Healthcare at ECOVIS, and Kathryn Dent, Workplace Relations and Safety Partner at HWL Ebsworth Lawyers, joined Macquarie Business Banking’s Senior transactional banker Matt Rose and over 100 healthcare professionals to discuss the changing healthcare landscape.

One particular ruling we spoke about was the enforced payment of $795,000 in payroll tax on medical practice operator Thomas and Naaz, which raised questions across the healthcare industry.1 The practice lost its case despite operating on a standard facility structure most practices have used for almost 40 years.

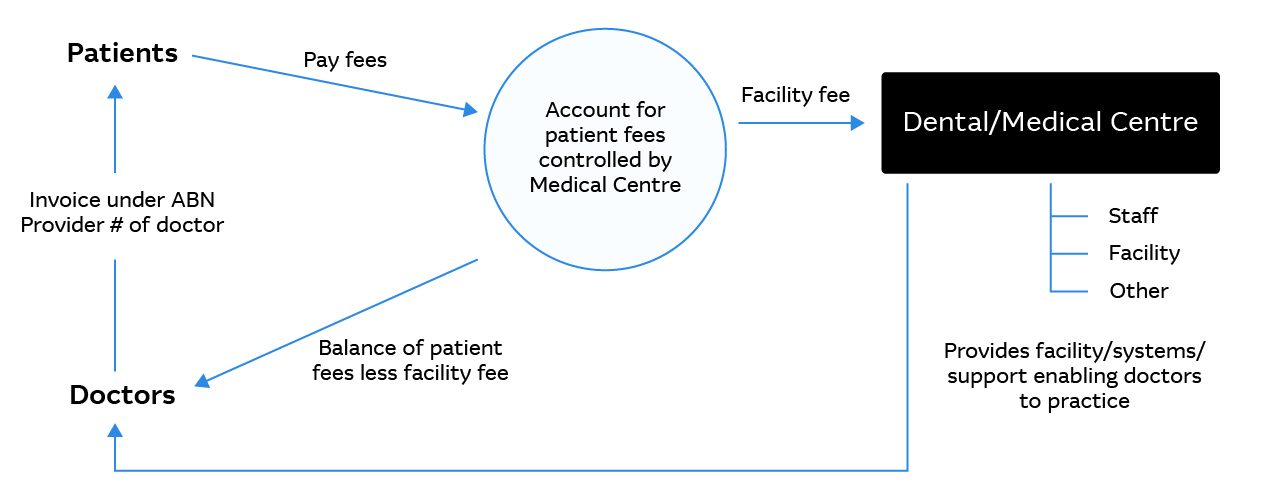

As Figure 1 shows, a medical centre or healthcare practice typically provides services, such as rooms, real estate, nursing staff and booking systems, to doctors who in turn provide services directly to patients. Doctors invoice patients under their ABN or provider number, and the centre collects patient fees and Medicare payments in a trust account on the doctors behalf. The medical centre then pays a portion of patient fees to doctors in return for their services while retaining the remainder as a facility fee.

Figure 1: A typical medical central payment model; source: ECOVIS

Figure 1: A typical medical central payment model; source: ECOVIS

The recent rulings indicate the Victorian and New South Wales State Revenue Offices (SROs) deem the share of patient fees paid back to doctors as subject to payroll tax. The courts and SROs also look at whether a healthcare professional is an independent contractor, generating their own profits, or whether a master / servant style relationship exists. Certain payroll tax carve outs also exist for doctors that are working across multiple practices. Businesses that do not have contracts in place that reflect an independent relationship between practitioners and centres will be almost certainly subject to payroll tax on these payments.

Given most healthcare practices operate on lean margins, the impost of payroll tax on these payments could have a severe impact on their business. During the webinar, Heath Stewart explained a practice with $3million in patient fees per year, disbursing $2million to doctors could face an annual payroll tax bill of almost $40,000 in NSW.

SROs have indicated they are commencing a programme to review all medical centres in Victoria and New South Wales in the coming years – so now is the time to seek expert advice on your situation.

“The State Revenue Offices in NSW and Victoria have made it very clear that they intend to conduct a review of every medical centre. If you are a practice operating under that typical model, it is a statistical certainty that you will receive a review from state revenue,” said Stewart.

He noted he is already seeing a lot of review activity across his client base. “For many practices those reviews do not go well. Especially if they don't have appropriate documentation or contracts in place.”

Finding the right solution for your practice

The first step is to understand the difference between independent contractors and employees and ensure your draft contracts clearly reflect this. Check existing structures reflect the intended relationships.

Independent contractors work in their own business, providing a service to others and negotiating their working arrangements and fees. Employees, on the other hand, work in a business – with set hours and workplace entitlements.

“We wouldn't expect to see, for example, provisions related to leave or employee benefits that are heavily skewed towards control – such as working hours – in an independent contractor agreement,” Kathryn Dent said.

She recommends practitioners provide their own equipment, charge GST on all invoices and can delegate work to and perform services for other principals. Ultimately if the contractor has their own business and is generating their own goodwill and profits they are less likely to be considered an employee. Providing services through an incorporated entity, rather than as a sole trader, also helps reduce the risk of falling under deeming provisions in superannuation and workers compensation laws.

“Arrangements with independent contractors should look different to employment arrangements,” said Dent.

The payroll tax laws are specific in terms of contracts which attract payroll tax liability such that systems and structures should be assessed as against the criteria which the Thomas Case recently highlighted. These types of contracts and models of work arrangements need to also be in consideration at the commencement of any working relationship so that the structures and systems support the intention of the parties and minimise any unintended legal consequences.

The tribunal decision has triggered many healthcare businesses to look at their operating and payroll models, and explore alternative options.

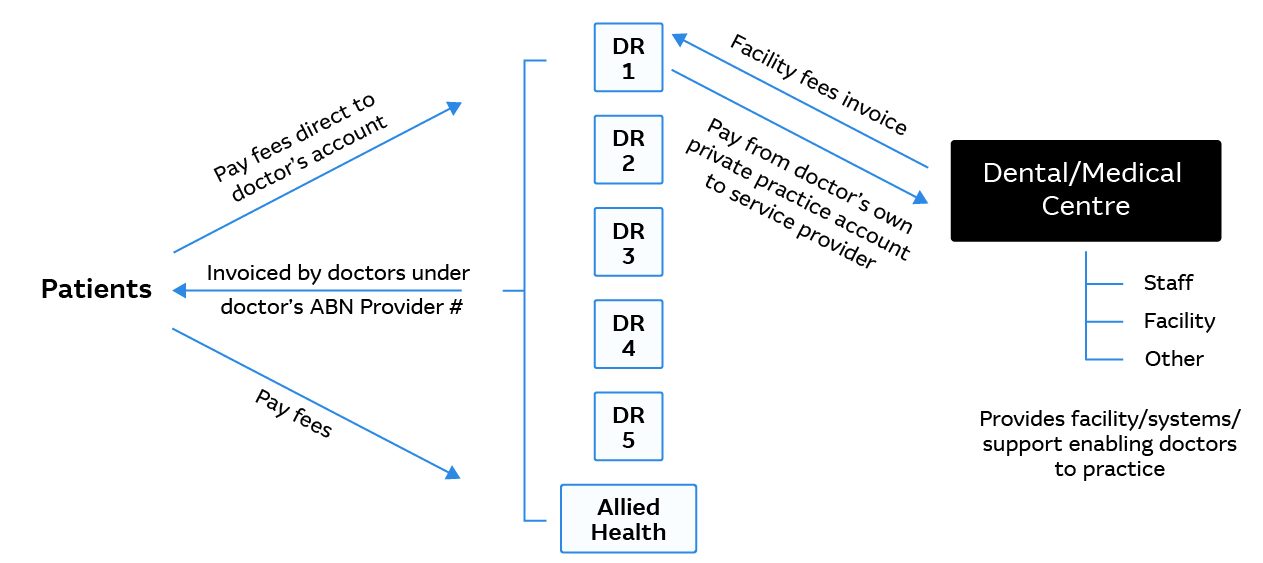

For example, figure 2 below allows doctors to receive patient fees and Medicare payments directly into their own bank accounts. They then pay facility fees to the centre for services provided.

Figure 2: Alternative payment structures for medical practices; source: ECOVIS

Figure 2: Alternative payment structures for medical practices; source: ECOVIS

However, an ‘arm’s length’ structure like this can create an administrative burden for practitioners, as well as cashflow pressures on centres relying on timely fee payments.

And in this scenario, a practice still could be subject to payroll tax.

“The New South Wales SRO has made it very clear that if you change your structure simply to avoid payroll tax, then the anti-avoidance provisions apply, and payments will still be subject to payroll tax,” Stewart said.

Bringing partners into the conversation

It’s important to consider the full ecosystem your centre operates in, including patients, staff and providers, as well as Medicare, private health funds, software solution providers, and your bank.

For example, Macquarie Business Banking can tailor its banking solutions to different healthcare practice models. Its specialist healthcare team has recently explored standardised direct debit solutions, and individual provider bank accounts, sub-account structures and trust entities for a range of clients. In addition, Macquarie Business Banking is exploring specialist healthcare technology and payment partners, and can work with them to support your unique payment requirements.

“Your practice will need to embrace the change these tribunal decisions enforce on the payment flows within the industry, and it will have a significant impact. I encourage leaders to lean in to driving that change from the top down,” said Matt Rose.

While there are some positive steps healthcare businesses can take to make sure they reduce the impact of a SRO review, there’s no one-size-fits-all solution. It’s a good idea to bring all your professional partners together, including your bank, accounting and legal teams, to help design and implement structures, processes and payment flows that meet your practice’s needs.

To discuss a viable plan for your practice, including potential payment flow solutions, contact your Macquarie Business Banking Relationship Manager or request a call today.