Following a short-lived blip last year, Australian house prices have recorded the fastest growth rate since 1988. But how long can this red-hot market last – and what does it mean for the real estate sector?

In this quarterly property market update webinar with CoreLogic, Head of Australian Research, Eliza Owen discussed the current market forces with Macquarie Business Banking’s National Real Estate Segment Head Domonic Thompson.

Macquarie upgraded its outlook for Australian housing prices in its March 2021 Investment Strategy Update, and is now expecting a trough-to-peak rise of around 20% by the end of 2022. However, while the impact varies across capital cities and regional areas, these growth rates simply may not be sustainable.

With record high values, Domonic noted the tremendous opportunities as well as pressures for Australia’s real estate agencies.

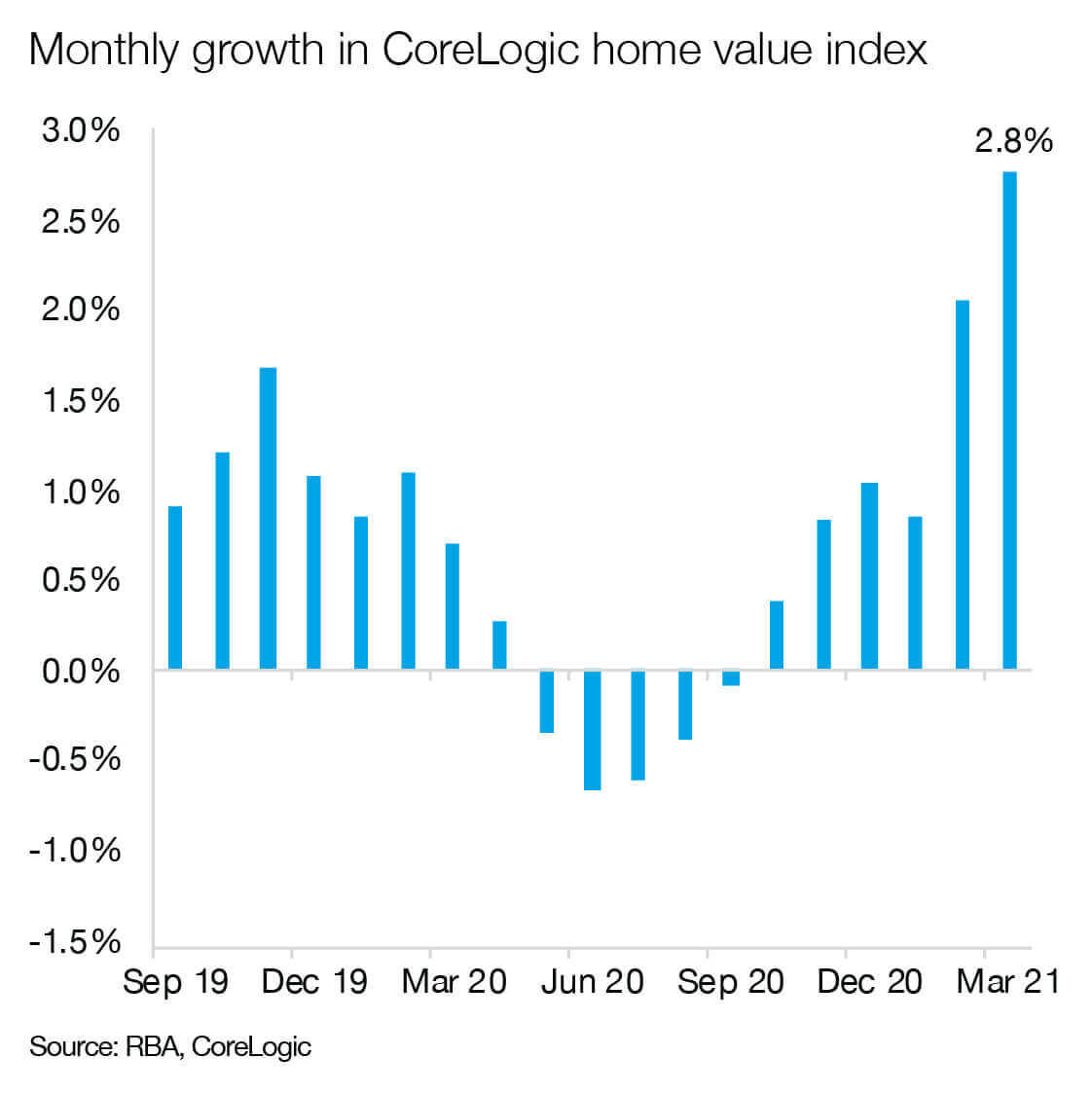

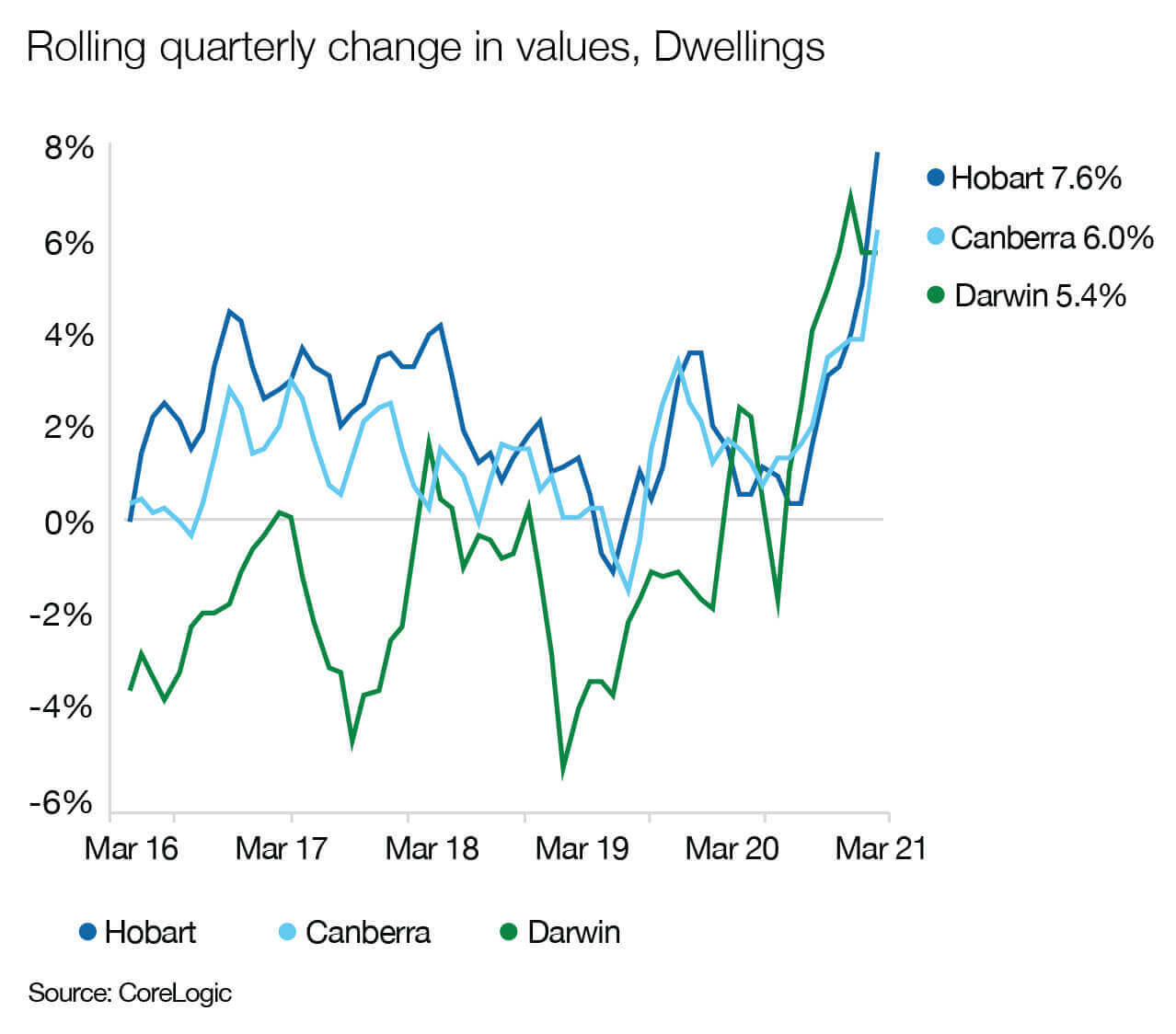

Australian house prices are rising at the fastest pace in 32 years

Australian house prices are rising at the fastest pace in 32 years

The perfect storm

This remarkable surge is thanks to three driving forces: record low interest rates, an unanticipated consumer confidence boost and low stock levels creating a sellers’ market.

Consumer sentiment in March was tracking about 12% above the decade average. “While not everything in the economy has been fixed coming out of COVID, we’re better off than we thought we might be. So people are more willing to commit to a high cost purchase like housing,” said Eliza.

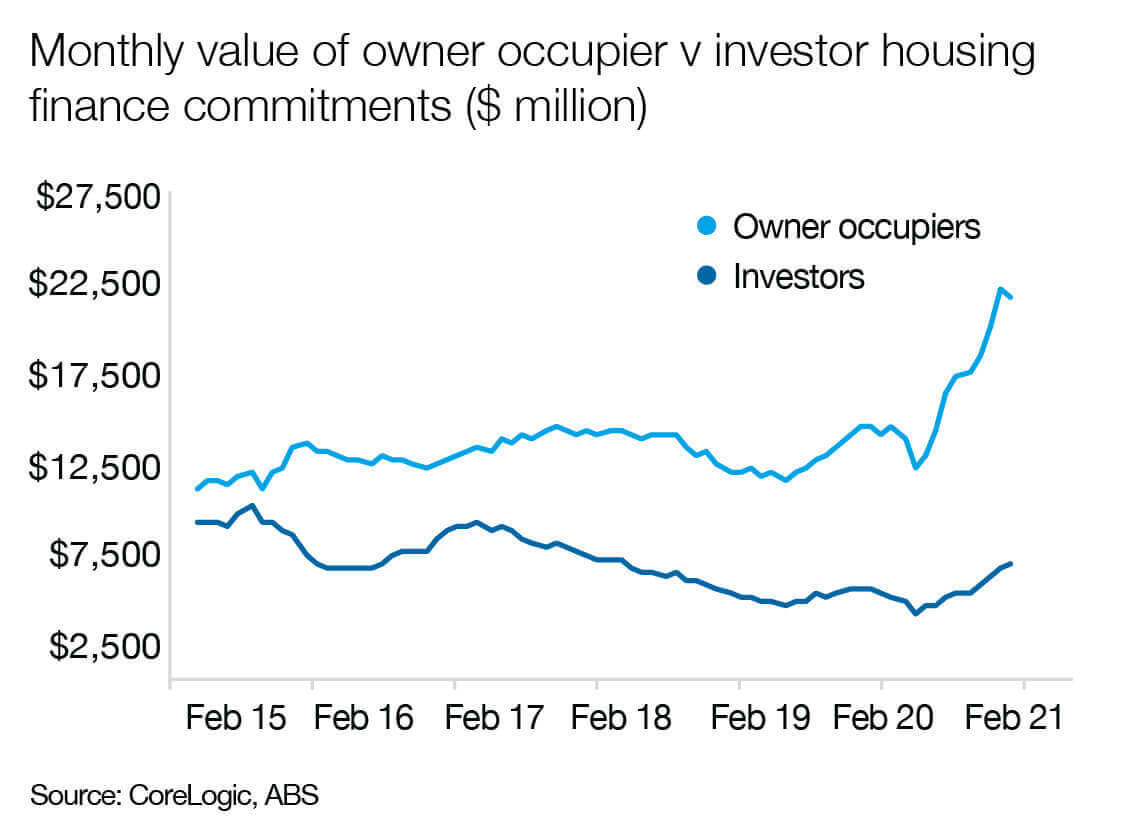

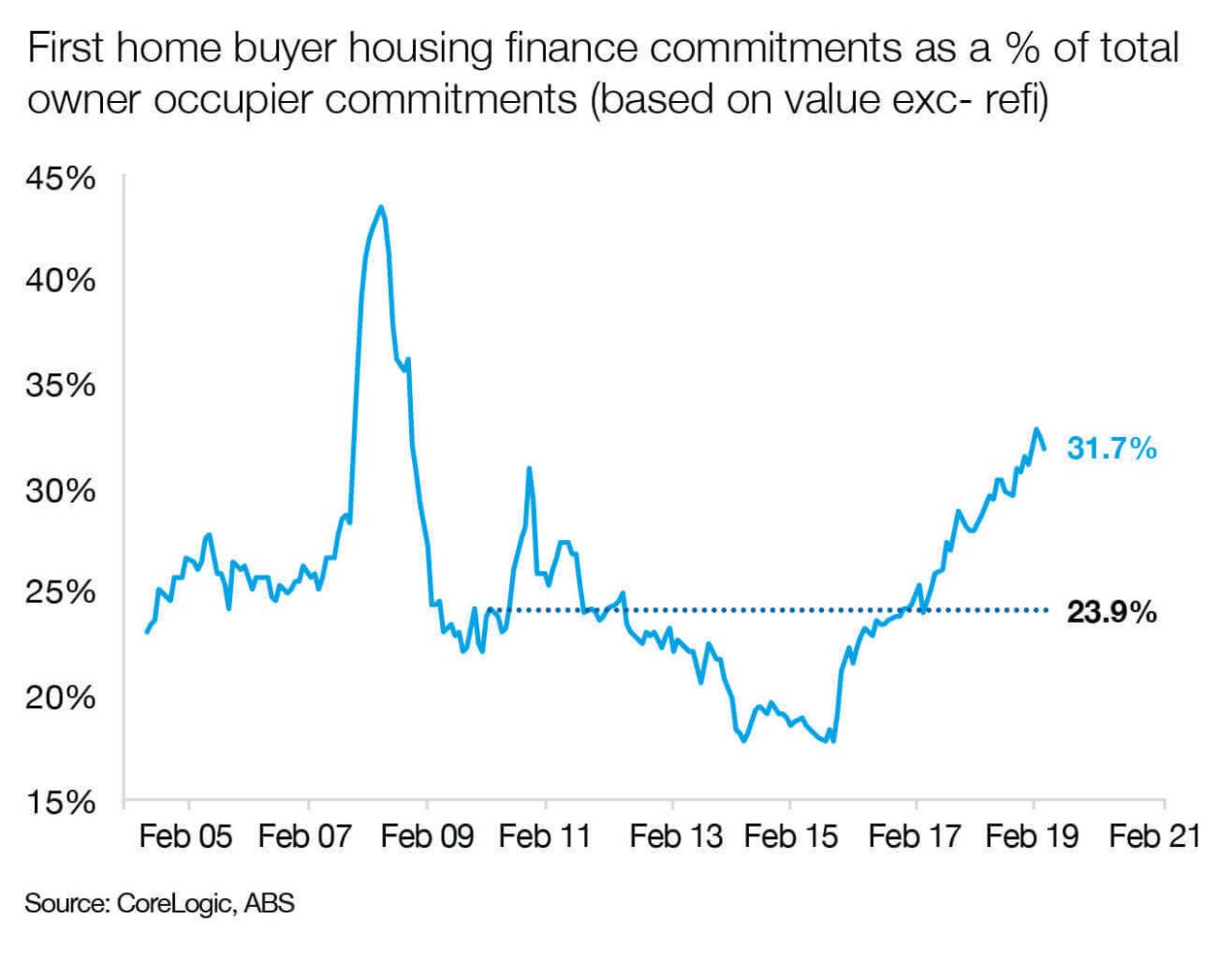

Until February 2021, owner occupiers dominated lending demand – as well as demand for houses over units. But more recently, there’s been a shift towards investors again.

“CoreLogic made that call last year: 2021 would be the year first home buyers started to back out of the market, and investor participation increased,” she said, noting the deposit hurdle will continue to be a barrier for buyers without property equity. Yet interest serviceability is falling as a proportion of income – and for about 28% of properties in Australia, CoreLogic data suggests it may be more affordable to service a mortgage than rent.

Investors are returning to the market, as first home buyers face affordability pressures

Investors are returning to the market, as first home buyers face affordability pressures

Domonic observed the impact of this shift between investors and first home buyers on property management.

“We are seeing some runoff on rent rolls – with consequences for clients securing loans against that asset,” he said. “First time buyers have been buying investment stock, while investors consolidated their positions. In some instances, rent rolls are trending backwards – or businesses need to peddle faster just to keep on an even keel.”

Meanwhile, advertised supply levels for sale remain at historic lows across most regions of Australia. With so much buyer activity, the imbalance between demand and supply is fuelling urgency – creating that upward pressure on prices.

Dominic suggested real estate agency owners will need to be careful about the business they take on while the market is running so hot.

“Not all business is good business, and we are starting to see price competition driving commission rates down,” he said. “Understand your Profit & Loss and empower your people to write business that maintains market share but won’t be detrimental for the bottom line.”

Trends across the states

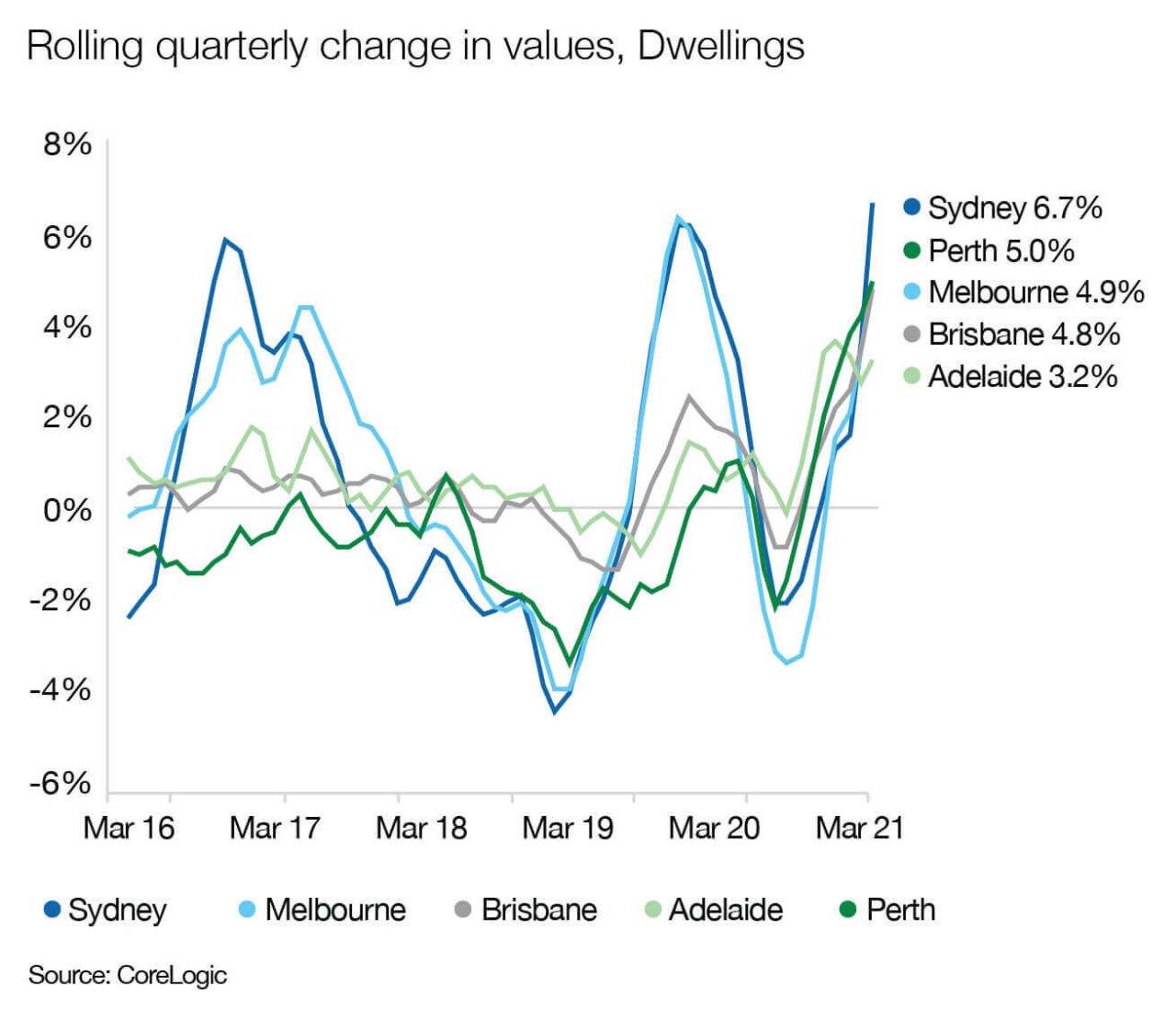

While we’re seeing solid upswings in values across all capital cities, Sydney is once again leading the charge – with many smaller capitals also showing a strong trajectory.

Historically, Sydney and Melbourne have the most volatility in their growth rates, and the pattern through COVID was similar. These cities are now close to their previous peaks – Sydney’s new record high is only 3% above July 2017.

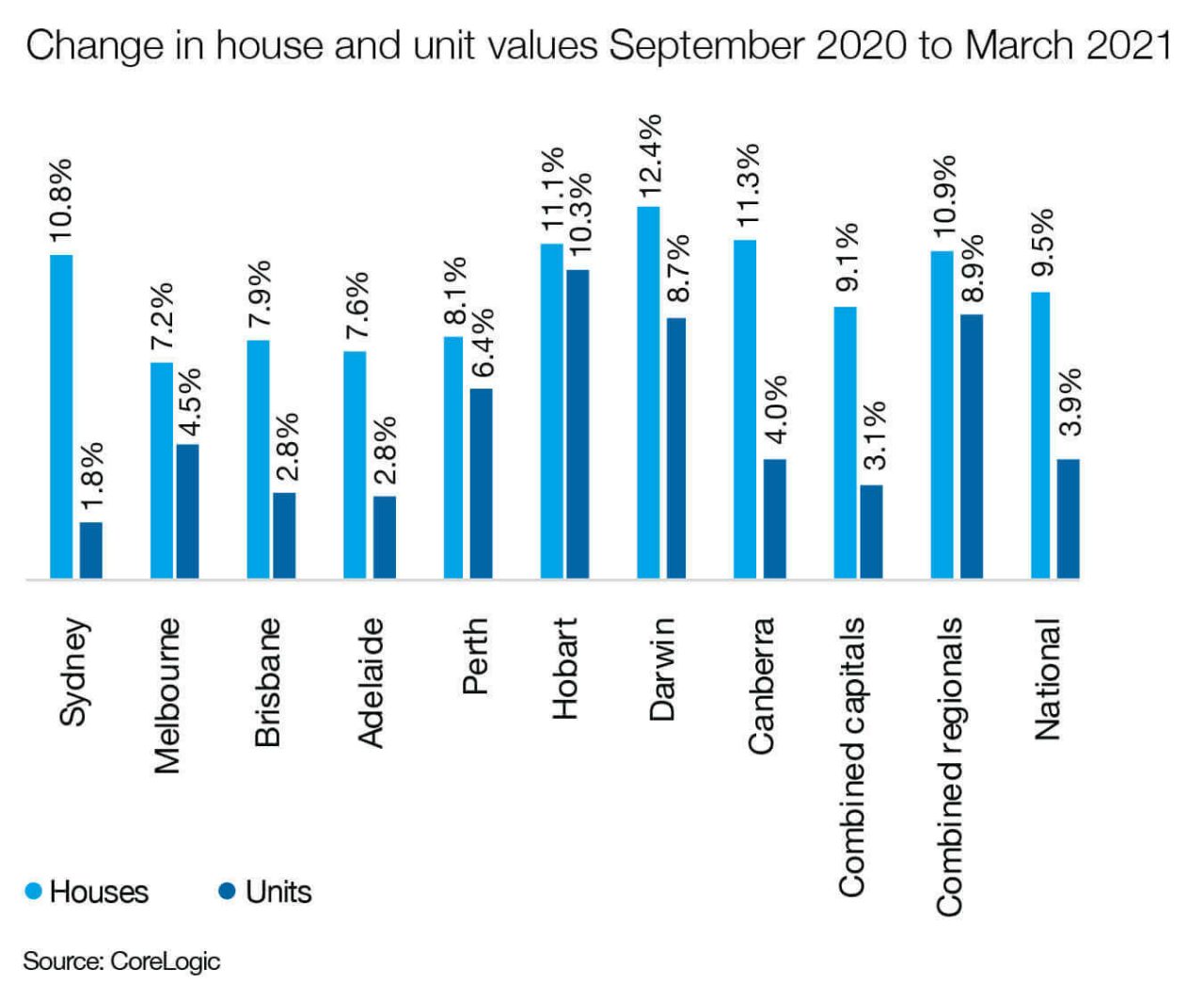

Strong growth rates across all capital cities, with Sydney leading the surge

Strong growth rates across all capital cities, with Sydney leading the surge

Canberra has shown the most consistent gains over 19 consecutive months, driven by a very strong labour market, high incomes and secure employment. Its dwelling values are now sitting almost 17% above the previous peak.

Melbourne’s apartment market remains a concern, with a higher proportion of unit valuations coming in under the contract price, and high numbers of apartments still under construction. “Rental market figures in Melbourne have also been disproportionately impacted by its exposure to overseas migration as a source of new housing demand,” said Domonic.

Internal migration trends through COVID have also been interesting to watch. Typically, net migration is also a result of people moving from regions to cities for work or study – but that didn’t happen at the height of the pandemic. While there is evidence of people ‘escaping’ to regional Australia, the top destinations for internal migration are similar to any given year – with the Gold Coast and Sunshine Coast still a preferred lifestyle choice.

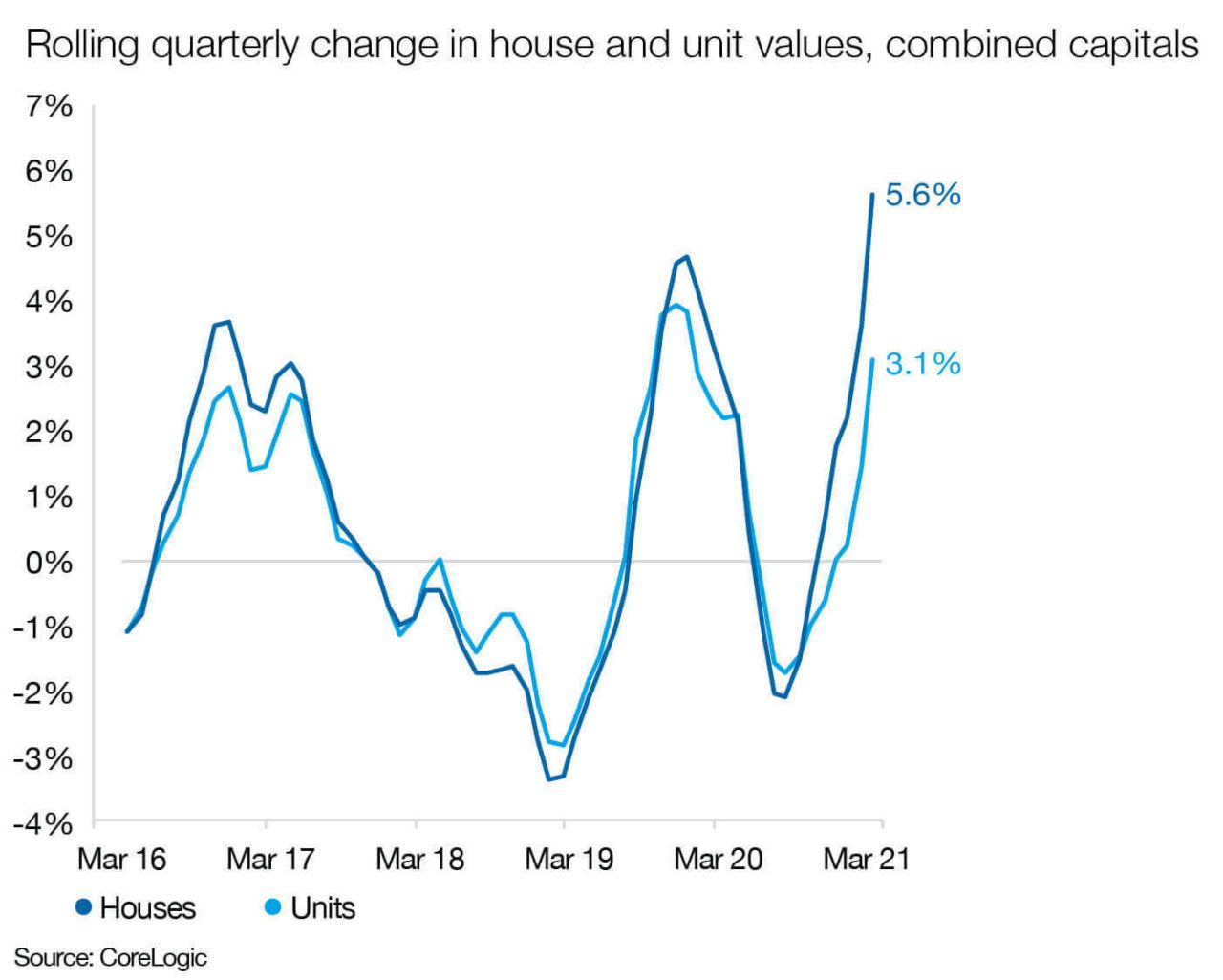

House value growth outstripped units, largely driven by owner occupier demand

House value growth outstripped units, largely driven by owner occupier demand

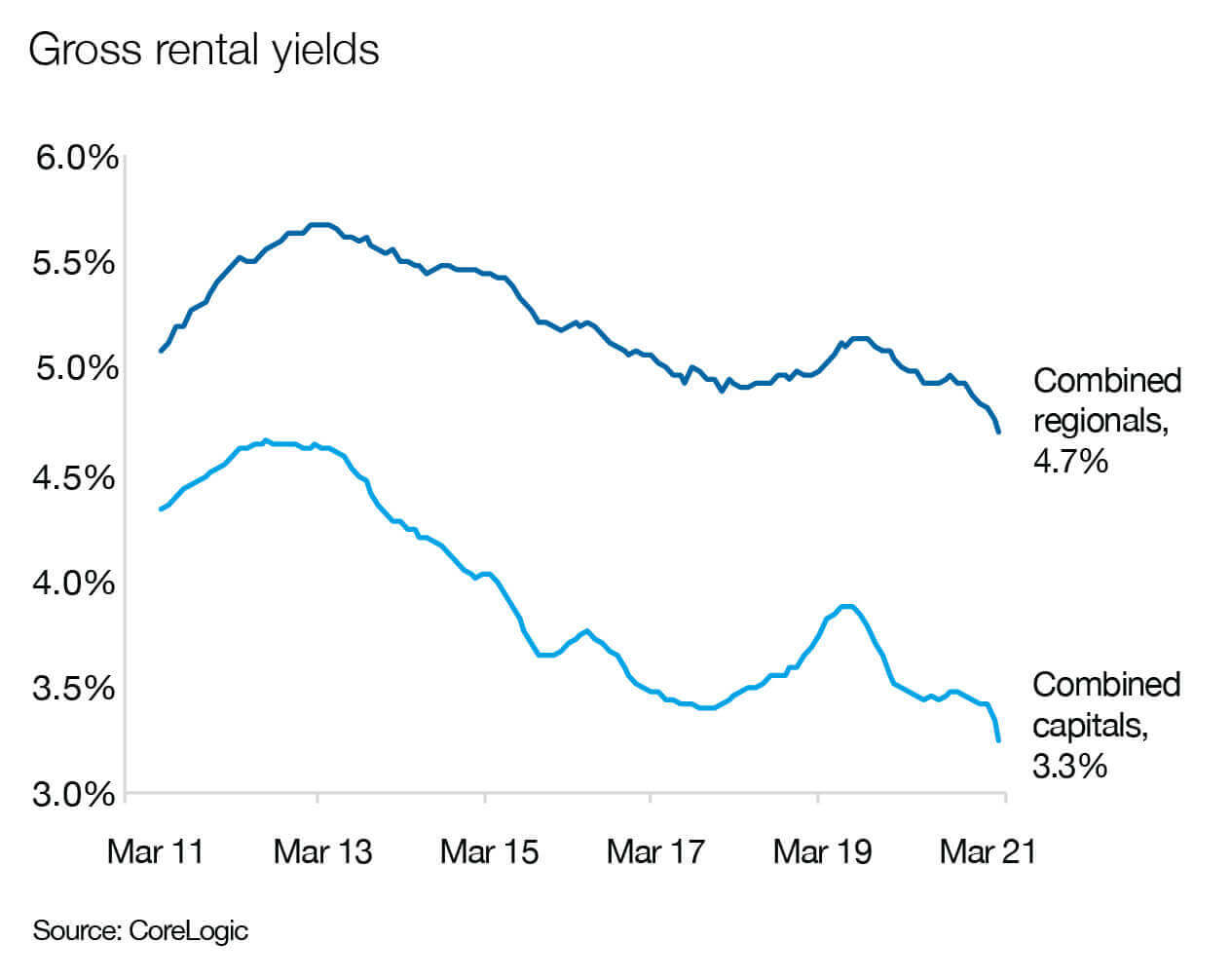

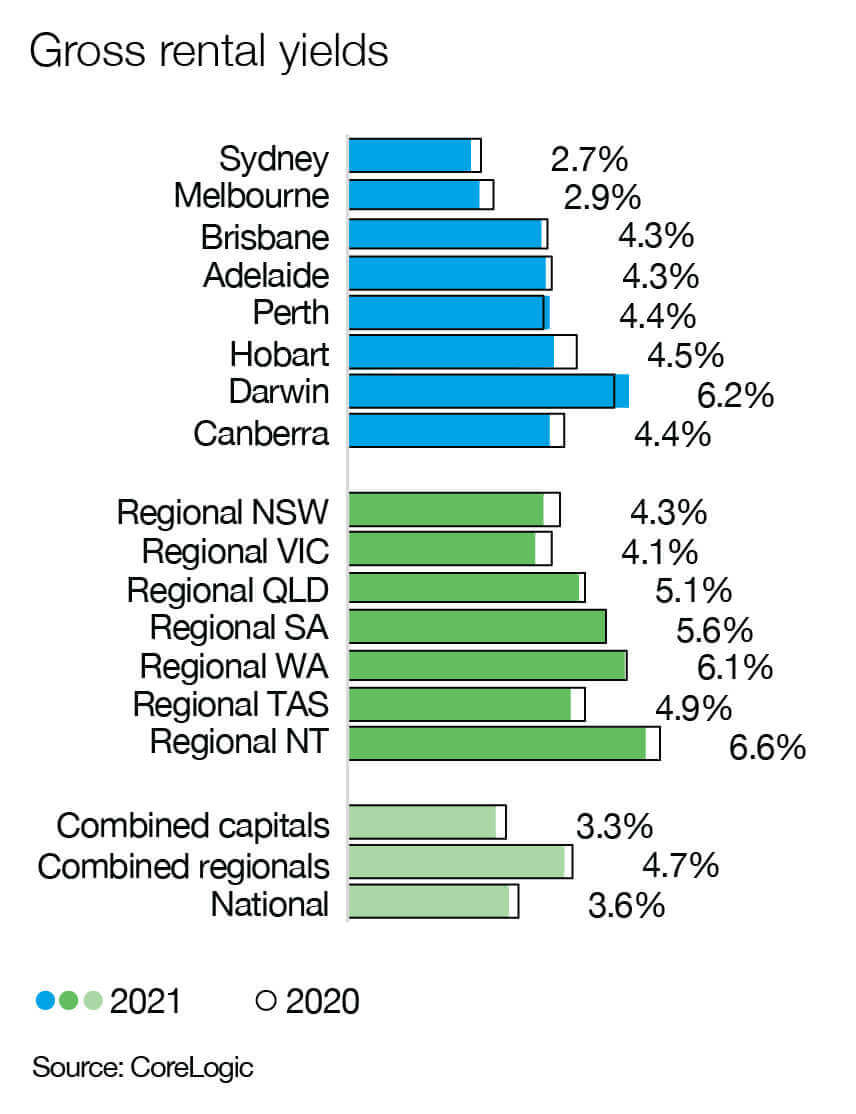

Rental markets are generally improving, even in areas badly impacted by COVID, depending on the type of stock. Sydney rentals recovered a little over the March quarter, and across Melbourne rentals are starting to steady. But gross rental yields in these two cities are still at record lows.

Taking care of business

While many economists predict[i] strong housing market conditions to continue for the next two years, we are not seeing any deterioration in lending standards – which means regulators are unlikely to step in. So real estate agents can expect valuations to keep on growing, even if that growth rate eases. “Sales may be the focus of attention and energy, but don’t ignore the property management side of your business, as it underpins consistent cash flow,” says Domonic.

He says it’s also just as important to take care of your team. “We’ve been through massive highs and lows over the last 12 months, and now everyone is working every hour they can to manage the workload,” he noted. “You need to take care of yourself and your people, to get through this.”

All these factors could make this a time of great opportunity for your business. As long as the opportunities are right for you, your team, and for your customers.