Reframe your perspective on insurtech’s value

In Macquarie Business Bank’s recent Insight Paper Thriving in Change, we shared the universal truths we believe most businesses are facing – and how these forces are impacting business value.

Technological change is now business as usual, and consumers won’t wait for you to catch up. Meanwhile, business models have been democratised: clients are deciding which businesses they want to deal with on the basis of their experience, rather than the ‘traditional way’ of doing things. And at the same time, market barriers have dissolved. New tech-enabled platforms are already solving client problems – in many cases faster, more cost-effectively and with a better experience.

I firmly believe that the current insurance landscape perfectly illustrates these three forces at play, and this year’s Insurtech Tour to Digital Insurance Agenda (DIA) in Munich showcased the very real impact of the emerging insurtech ecosystem and opportunities for incumbents.

In partnership with Insurtech Australia, Macquarie led a diverse delegation of 40 people including insurers, brokers, underwriting agents and insurtech start-ups to London and Munich in October 2018. Through a series of powerful presentations in London, as well as the conference itself, we saw how incumbents and insurtechs are already combining their strengths.

Australia’s insurtech ecosystem is still young and growing quickly. According to Insurtech Australia’s recent report with EY, the average age of an Australian insurtech is just three years – and 81% believe incumbent players aren’t doing enough to collaborate with them to drive innovation.1

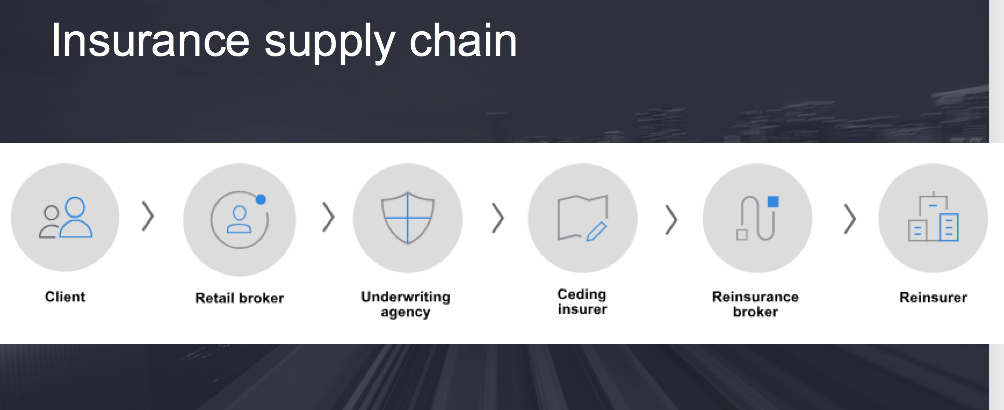

Why does this matter? We’re already seeing how effective partnerships allow both groups to thrive in this new world of insurance. Traditional players need to find new models for underwriting, distribution and claims. Insurtechs are ready to add tangible client value at various points in the supply chain.

But only if we bring their very different strengths together – the processes, resources and potential test market of the incumbent, and the agile digital talents of the start-up.

Build together, or buy in?

In these more mature markets, it is clear that capital is hungry for opportunities – and major insurers are investing in different ways.

For example, Greg Brown of strategic consultancy Oxbow Partners described a ‘vibrant’ global ecosystem that includes marketing and distribution (such as Bought By Many and NEOS), data, pricing, processing, claims and back-office.

He said incumbents are using a range of innovation models – from innovation teams (such as Lloyds Labs, which we visited in its first week of operation) to incubation (Allianz X) and investment (Allianz Ventures and XL Innovate). QBE’s partnership with Cytora is just one example: by using AI to price commercial insurance risks, it’s already making a difference of up to 18% on loss ratios.

For insurance brokers, it’s just as important to have a partnership strategy in place. Brown suggests seeing insurtechs as service providers, not just products to push or integrate – because then you can also benefit from the technological expertise and talent they bring as a partner.

The growing risks of complacency

Munich RE’s Dr Tobias Farny described a “pyramid of change” with concrete opportunities for brokers. Technology can be used to improve client interfaces, and data to remove form-filling friction, while expanding risks (such as cyber threats or pandemics) will demand new product streams.

But at the peak of this pyramid, disruptive technology such as AI and virtual risk carriers could remove the need for more inefficient players in the complex insurance value chain.

EY’s Ian Meadows put it bluntly: “There are too many mouths to feed in the $600billion wholesale commercial insurance model.” As we’ve seen in other markets, when clients don’t see the value in your proposition and costs become unsustainable, they’ll look for alternative solutions. He believes paper-based data flow is stagnating the industry.

What’s next?

Globally, the insurance ecosystem is already blurring its borders with other sectors. German fintech Treefin’s Andreas Gensch shared two examples of cross-industry models, including a partnership between Zurich and safety technology firm Abus which combines risk mitigation or prevention with discounted products.

When insurance is embedded into a broader purchase decision in this way – the right product at the right time for the right price – how will the role of the broker remain relevant?

I believe it is still based in the very human need for advice-led relationships. One thing that became clear as I watched more than fifty insurtech pitches at DIA is that the ones that resonated had a strong sense of ‘why’. Beyond the smart features of their tech, they could clearly show how it makes the client experience better.

This tangible end user focus is sometimes a missing ingredient. But it’s a strength brokers, who know their clients better than anyone, can bring to the evolving insurtech ecosystem.