Cash injection to provide short-term cost relief

We review the Australian Federal government’s 2022/23 budget and assess its implications for Australia’s financial markets.

- This is a pro-growth budget that emphasises cash payments to alleviate near-term cost of living pressures on consumers. These measures are mostly temporary in nature but will provide crucial near-term relief where required.

- Despite a better-than-expected fiscal position, there is a degree of restraint with the budget with ongoing but declining deficits. We identify 4 key areas of policy support and focus: 1) cost of living; 2) infrastructure; 3) health, education & environment and 4) defence.

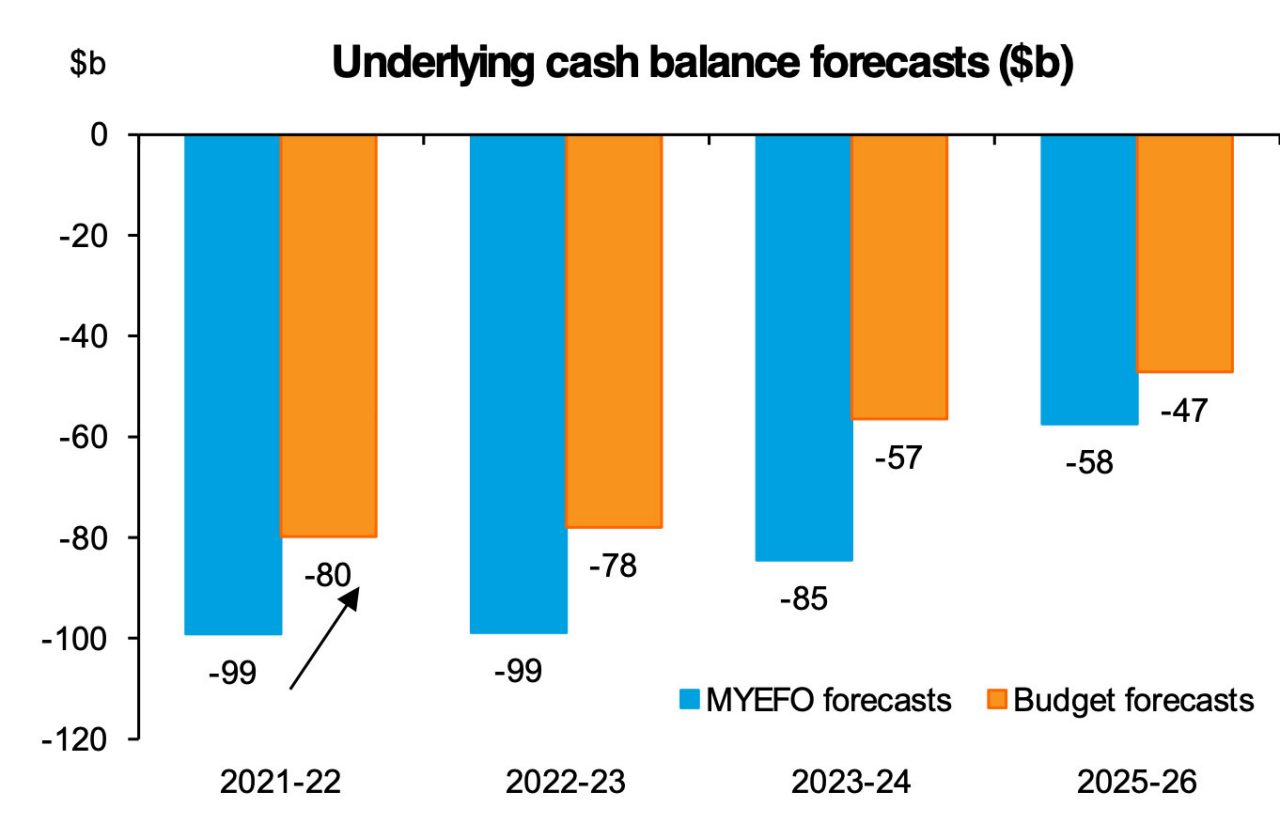

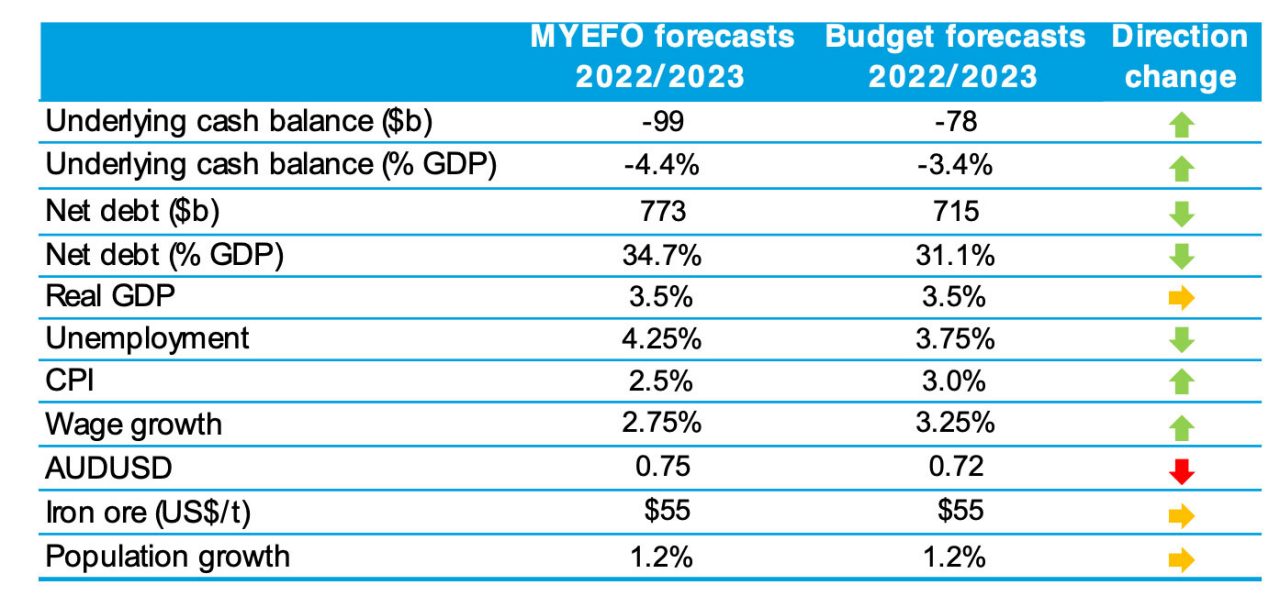

- Budget deficit shrinks: The combination of a strong domestic economy and uplift in commodity prices supported a much-improved budget position than forecast in December. The budget’s cash balance is now expected to be a deficit of $78 billion in 2022/23, a solid improvement on the $99 billion December MYEFO forecast.

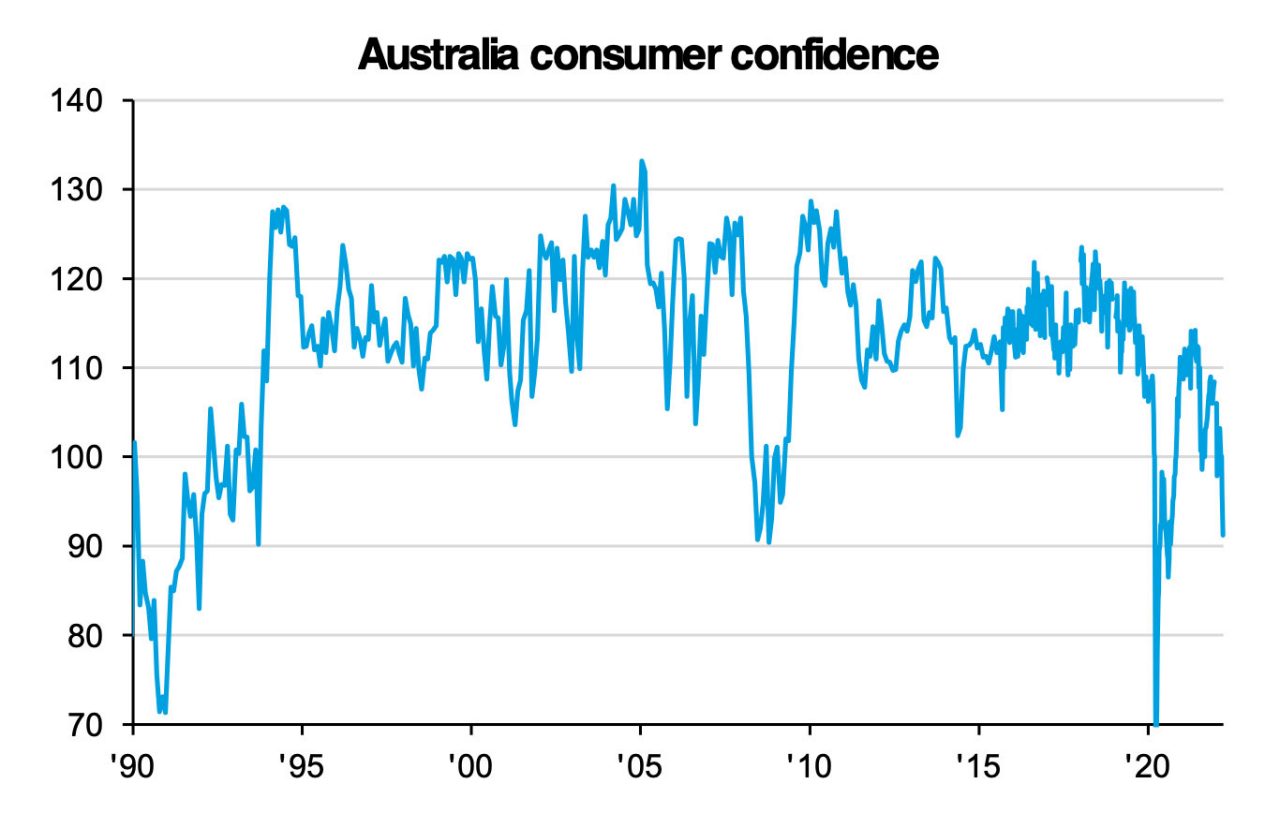

- A boost for consumption: This is a positive budget for consumer spending with immediate fuel excise cuts and cash handouts for low-and middle-income earners. This is a short-term sugar-hit, but will be welcomed as consumer confidence has recently declined sharply.

- Which areas lost out? The temporary nature of expenditures in this budget means areas requiring long-term structural reform were underrepresented. There was little for the transition to a more sustainable economy (e.g. electric vehicles) and regions won out at the expense of CBDs (which need to be revitalised).

- A boost for consumption & Infrastructure stocks: Budgets are not typically market moving events and we expect this one will be no different. While it is pro-growth and will boost consumer spending, the one-off nature of the payments means there will be no long-term benefits for the consumer sector. At this stage, while the cash splash may add to inflationary pressures, the market has already priced in a much earlier than expected start to rate hikes vis-à-vis the RBA and so we don’t think this is a major headwind.

- Consumer & infrastructure stocks are the major beneficiaries of this budget. Key stocks Macquarie prefers include Premier Investment (PMV), JB Hi-Fi (JBH), Coles (COL), Boral (BLD) and ADBRI (ABC).

Federal Budget 2022/23

This budget was a notable shift from 12 months ago. Last year the recovery was fragile, the economy was transitioning away from JobKeeper, unemployment was >6% and the vaccination effort was yet to start in earnest. Now, the economy has strong momentum (despite Omicron), full employment is in sight, wages are growing, inflation is widespread, and commodity prices continue to surprise to the upside. Given this much more favourable backdrop the focus has shifted from stimulating a nascent recovery to near-term cost-of-living support for consumers and budget repair.

The budget position was strongly ahead of Treasury’s December forecasts in the Mid-Year Economic and Fiscal Outlook (MYEFO). The budget is expected to remain in deficit over the forecast period, supporting the economy’s rebound, but with smaller deficits than previously expected.

A much better than expected budget outcome

Source: Macquarie, MWM Research, March 2022

Source: Macquarie, MWM Research, March 2022

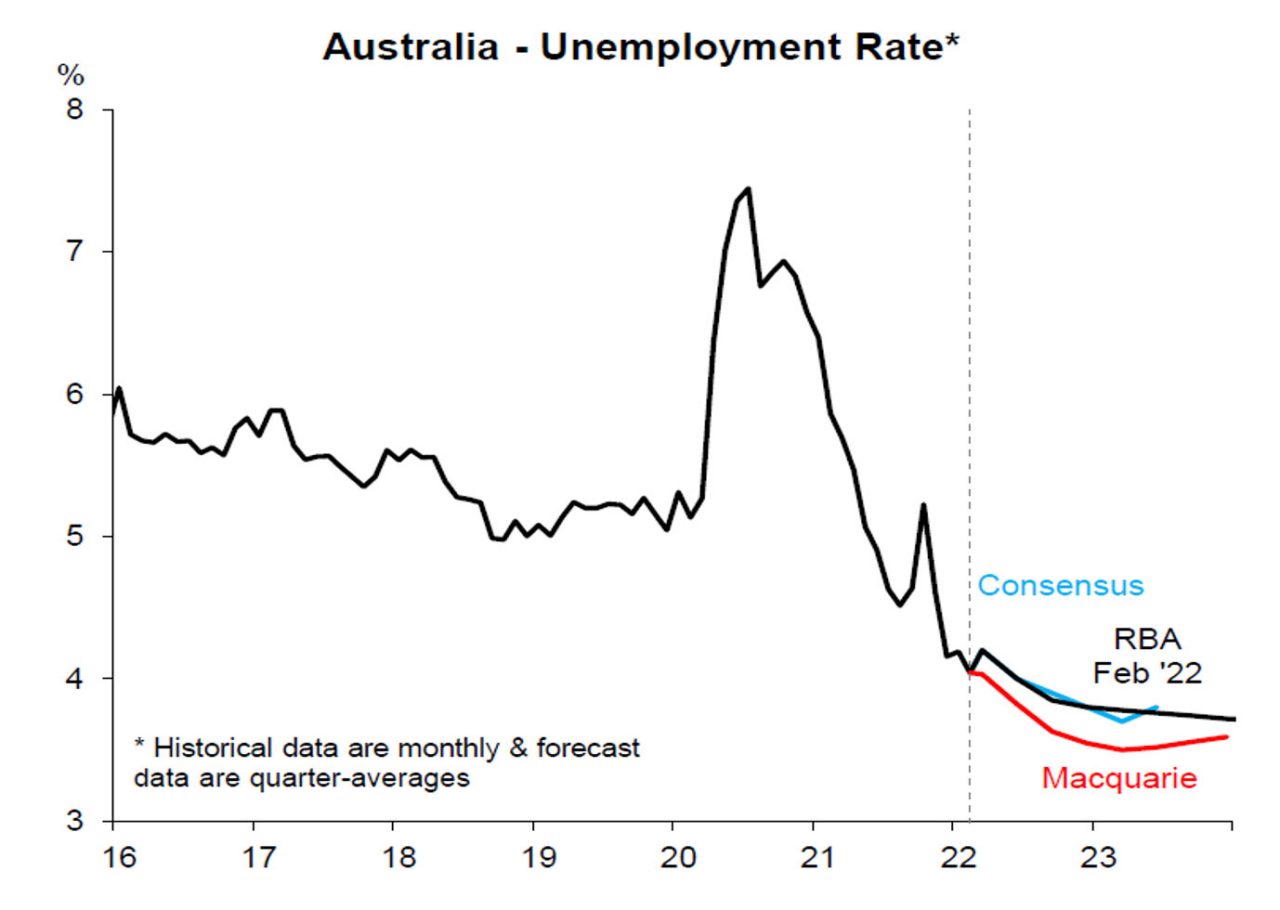

Recent budgets have prioritised supporting businesses and consumers through COVID-19, jobs growth and business investment to stimulate a domestic recovery. This has largely gone to plan with the economy in rude health and unemployment likely to hit the lowest levels in 50 years. Strong jobs growth boosts the budget’s bottom line via a higher tax intake while reducing welfare payments. The jobs recovery has been well ahead of forecasts. The unemployment rate is already at 4% with Macquarie expecting ~3.5% later this year. Similarly, wage growth is to increase to +3.25%pa, the strongest levels in a decade.

The economy is nearing full employment

Source: Macquarie, MWM Research, March 2022

Source: Macquarie, MWM Research, March 2022

Fiscal repair is now firmly on the agenda. Last year, the government was committed to getting the unemployment rate below 4.5% before considering fiscal repair. With this now achieved, the shift to fixing the balance sheet is very much on message. The approach here is to focus on supporting economic growth, rather than drastically cutting expenditure or introducing new taxes. As a result, we don’t expect the shift to budget repair to be as negative for consumer or business sentiment as the approach taken in 2013/14 which saw confidence collapse. We see no threat to Australia’s AAA credit rating from this approach with the ratings houses already indicating austerity measures are not required nor desirable.

Consumer confidence has declined rapidly as costs rise

Source: Macquarie, MWM Research, March 2022

Source: Macquarie, MWM Research, March 2022

Treasury now forecasts a much-improved outlook for the Australian economy. Growth will be stronger, full employment will be reached sooner and wage growth will be higher. A higher tax take from the stronger economy will translate to lower deficits and debt levels than expected in only December. Commodity forecasts continue to be very conservatively set.

Treasury forecasts a robust recovery

Source: treasury.gov.au, MWM Research, March 2022

Source: treasury.gov.au, MWM Research, March 2022

We review the major policy initiatives below.

1. Cost of living pressures

This budget was squarely focused on easing the burden of recent prices across the economy.

Key initiatives include:

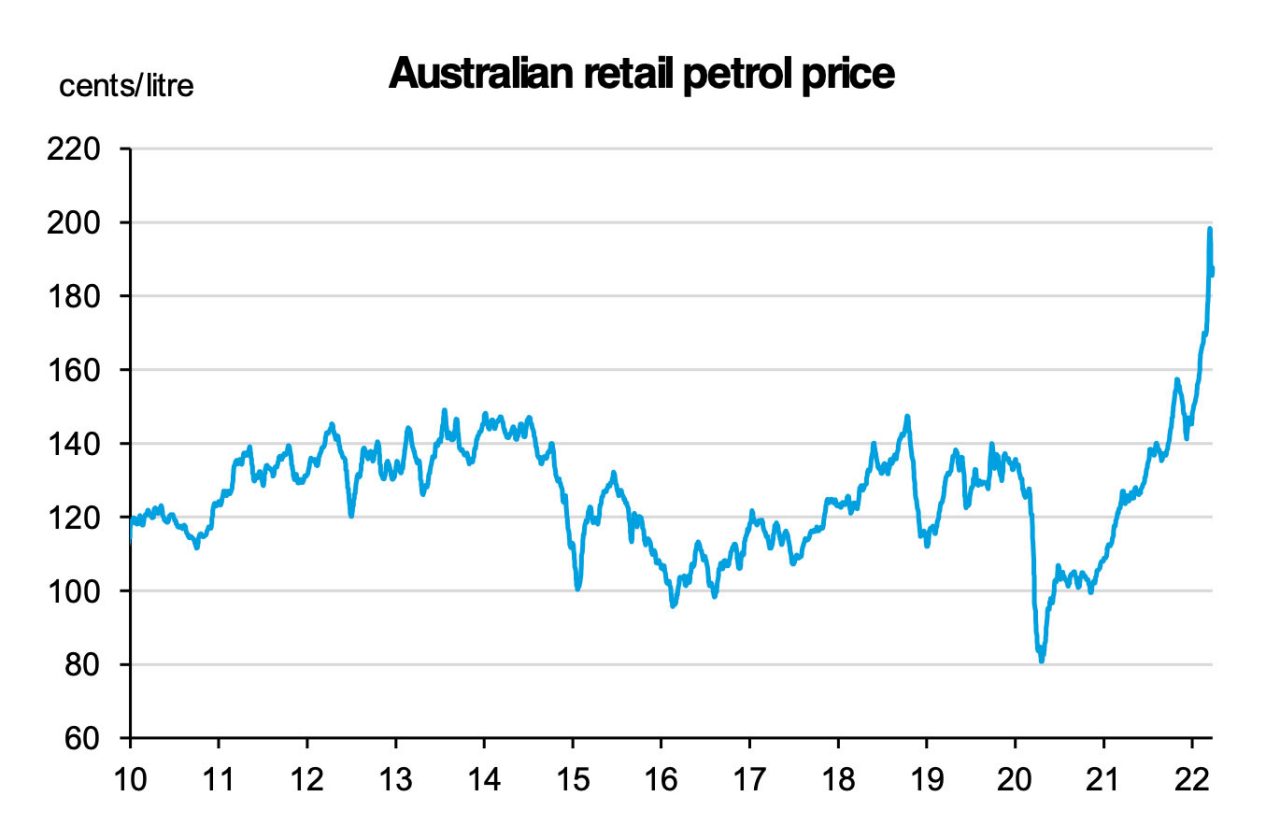

- Fuel excise cut – Fuel excise will be cut by 50 per cent (from 44.2 to 22.1 cents per litre) for 6 months commencing 30th March at a cost of $5.6 billion.

- LMITO – the low-and middle-income tax offset (LMITO), which was expected to not feature in this budget, will instead be bumped up from $1080 to $1500 to assist with cost-of-living pressures, at a cost of $4.1 billion.

- Cash handouts – The Government will provide a one‑off, income tax-exempt payment of $250. This payment will help 6 million people (more than half of whom will be pensioners) at a cost of $1.5 billion.

- Home guarantee scheme – the scheme, which supports first home buyers into the housing market with only a 5% deposit, will be expanded to 50k places annually and has also been made permanent.

Consumers will receive immediate relief from petrol prices

Source: Infrastructure Australia, MWM Research, March 2022

Source: Infrastructure Australia, MWM Research, March 2022

2. Infrastructure

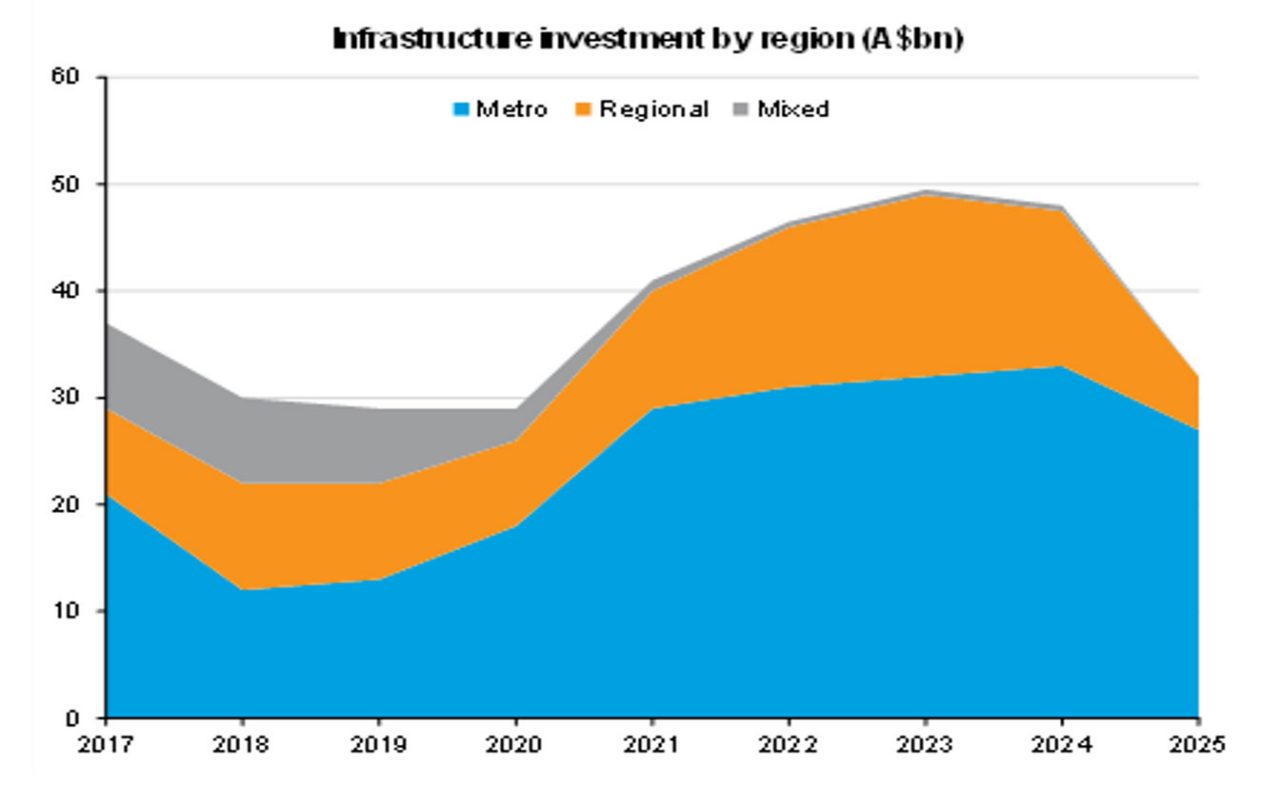

Infrastructure spending features heavily again with $17.9b committed to high priority projects including:

- Hells Gate Dam - $5.4b to build the far-north QLD project

- Melbourne intermodal terminal at a cost of $3.1b

- Outback way - $0.7b to seal a further 1000km on roads

- NBN upgrades - $0.5b to upgrade the NBN’s fixed wireless network providing much faster speeds in rural and remote areas.

Infrastructure investment in regional areas to increase

Source: Infrastructure Australia, MWM Research, March 2022

Source: Infrastructure Australia, MWM Research, March 2022

3. Health, education and environment

Key initiatives include:

- Domestic vaccine facility – the government will co-fund the development of a domestic vaccine manufacturing and R&D hub with Moderna at a cost of $2 billion. Expected to be operational by 2024 and ensure vaccine supply.

- NDIS users: Spending on the National Disability Insurance Scheme has increased by $40 billion (to $158 billion) over the forward estimates.

4. Defence spending

The Ukraine war has necessitated a strategic uplift in defence spending. Major initiatives announced included:

- Boost the defence force with $38b to increase personnel by 18,500 by 2040

- Future naval infrastructure funding of at least $10b including an east coast submarine base

- Armoured vehicles to receive funding of $3.5b

Equity market takeaways

This was a mildly pro-growth budget, but nothing compared to those announced through the pandemic. But, for the equity market, the reopening of the economy alongside further upward momentum in global growth, was likely to be the key tailwinds rather than additional policy support from the federal government.

Traditionally, budgets don’t have a major or a prolonged impact on the equity market and we don’t see the current combination of policies as anything different. There will be a boost to consumer spending and those areas leveraged into infrastructure may also see a small tailwind, But we don’t see either as being long dated positive drivers given the one-off nature of the cash payments and because the infrastructure sector is also facing structural constraints that are limiting new project starts.

It is hard to gauge how the additional cash payments will flow through. This is because excess savings already stood at around $240bn and was also there as a backstop for spending. In addition, if consumers feel that cost of living concerns will linger, then they may not be so willing to spend their handouts as they arrive.

At the end of the day, the equity market is being held up by a reasonable earnings outlook alongside still very favourable monetary conditions. We might see some evidence of earnings upside but given the momentum in commodity stocks (energy and materials), it’s unlikely that this is broad enough to drive a significant improvement. On the negative side, there is some risk that additional spending will force the RBA to move more quickly in raising rates. This would clearly be a headwind for the market, but we think market pricing was already factoring in a much earlier than expected start to the rate hike cycle than the RBA was forecasting.

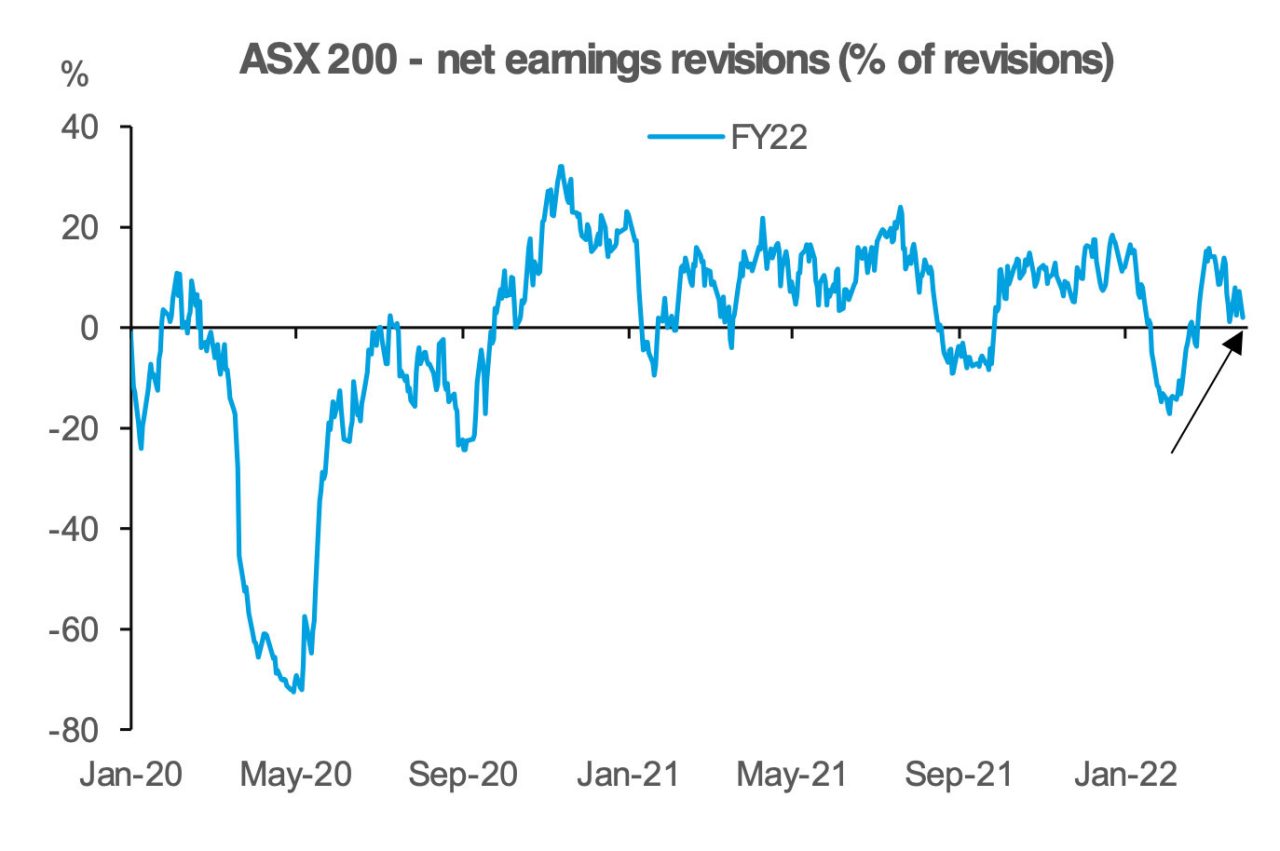

Earnings revisions picking up in line with economy

Source: FactSet, MWM Research, March 2022

Source: FactSet, MWM Research, March 2022

Relative to previous years we see only a small set of sector beneficiaries. The cash handouts were the biggest surprise in the budget, as it was uncertain whether the LMITO would feature. This should be welcome news as the retail sector looks to pass through price hikes. Other areas that received significant spending, such as defence, are not well represented on the ASX.

- Consumer – Premier Investment (PMV), JB Hi-Fi (JBH), Harvey Norman (HVN), Coles (COL)

- Infrastructure – Boral (BLD), ADBRI (ABC), BlueScope Steel (BSL), Ventia Services (VNT), Downer (DOW)

Macquarie WM Investment Strategy Team