interest rate applies for disclaimers

For basic owner-occupied home loans with principal and interest repayments.

Get the features you deserve and switch to a Macquarie home loan.

You could save on your home loan with our competitive rates and low fees.

Get a fast response on your home loan application and refinance with confidence.

Be in control of your home loan with flexible loan options including split loans and up to 10 offset accounts for each of your variable interest rate home loan accounts.

Settle for nothing less than great rates and low fees.

Save over the life of your home loan with access to great rates and no hidden fees or charges.

Turnaround times that won’t leave you wondering.

At Macquarie, we pride ourselves on having market-leading turnaround times so you can make your next move with confidence.

When it comes to your home loan, we’re flexible.

With fixed rates for more certainty, variable rates, and offset accounts to reduce the amount of interest you pay - you’ve got options.

An award-winning digital app.~

Plan your future, keep track of your investment, and stay in control. Managing your home loan has never been easier from the palm of your hand.

The refinance process for each lender may be different. To refinance to a Macquarie home loan, you can apply online or speak to one of our specialists. For more information on the process, visit our help centre.

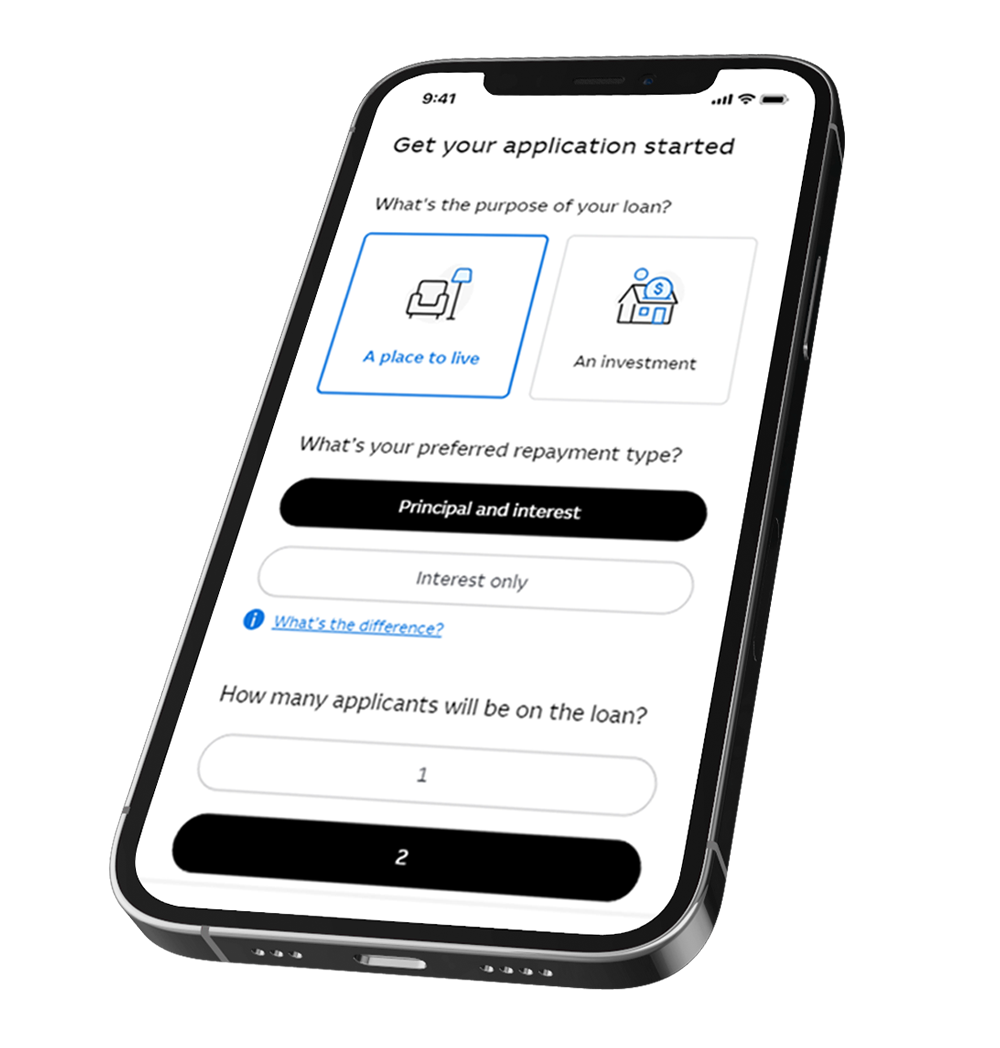

To help you complete your home loan application, make sure you have the following information on hand:

You can start your application now, save your progress, and come back to it later if you need more time or additional information

A home loan specialist will review your application and contact you within 1-2 business days.

Resume your refinance application at any time by securely logging in here.

The rates shown in the application are accurate based on the information provided and as at the time of applying. All rates are subject to approval and may vary depending on a formal valuation of your property or other rate changes announced during the application process.

A Home Loan Specialist will review your application and call you within 1-2 business days after submission. If you’d like to make an update simply let them know during this call.

Our team of home loan experts are here to help. Request a call by completing the form and we'll typically make contact with you within 1 business day.

If you're an existing customer looking to make changes to your home loan, please reach out to us via Q in your Macquarie Mobile Banking app or Macquarie Online Banking.

Support for customers

This information is provided by Macquarie Bank Limited ABN 46 008 583 542 AFSL and Australian Credit Licence 237502 and does not take into account your objectives, financial situation or needs. You should consider whether it is appropriate for you. Lending criteria, fees and T&Cs apply.

Rate applies for new loans when you borrow up to 60% of the property value with a principal and interest repayment variable rate loan. Subject to change without notice.

The information in this calculator is by way of example only and is not a prediction or professional financial advice. Calculations are not forecasts, but may assist you in making your own projections. Subject to law, Macquarie will not be liable for any loss or damage caused by your use of the calculator. The information in the calculator does not constitute an offer to lend or imply the product is suitable for you.

Variable rates apply to new loans with a variable rate loan account and will vary based on the amount you’d like to borrow, relative to the property value and the repayment type you choose e.g. principal and interest. Fixed rates apply to new loans with a fixed rate loan account. Rates reflect our current advertised rates and are subject to change without notice in the application process.

Fixed rate loan accounts may be subject to significant break costs. Please refer to the loan contracts for terms and conditions regarding break costs. At the end of the fixed rate period, the interest rate will revert to the discount variable rate applicable at that time.

The comparison rates are based on a loan for $150,000 and a term of 25 years. WARNING: This comparison rate applies only to the example or examples given. Different amounts and terms will result in different comparison rates. Costs such as redraw fees or early repayment fees, and cost savings such as fee waivers, are not included in the comparison rate but may influence the cost of the loan.

Our digital banking platforms are part of why we were awarded Money Magazine’s Bank of the Year 2023/2024.

Home loan information and interest rates are current as at 2 April 2026 for new loans only and are subject to change.