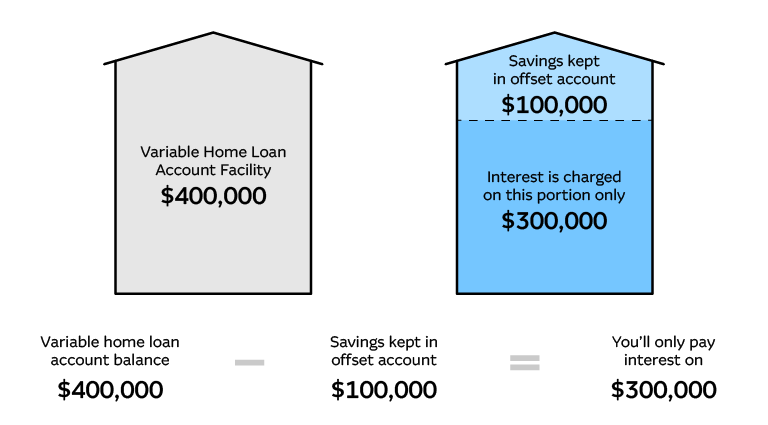

1. Place excess savings into your offset account

If you inherit a lump sum, or have a term deposit, you may want to consider placing those savings in an offset account. While it might seem counterintuitive if you're used to locking away your savings into a high interest account, an offset account can be beneficial. This is because your home loan interest rate may be higher than the rate on your savings account, and you'll also pay income tax on the interest you earn.

You can also set up regular savings payments into your offset account – so if you're used to putting away money for an annual holiday, you can still do that with an offset account and withdraw the money when you're ready to pay for your trip.

2. Deposit your salary into the offset account

If you get a debit card with your offset account and online access to payments, consider using it as your default transaction account and let your employer know to make salary payments into the offset account. Every dollar helps.

Interest is calculated daily on an offset account, so even if the balance fluctuates with your day-to-day transactions, you'll still be offsetting your interest.

3. Combine your offset account with credit card payments

The more money you can keep in your offset, and the longer you keep it there, the more you will save. So, if you’re disciplined, you could use a credit card to defer everyday expenses by utilising the interest-free payment period.

It is important to always pay off the full balance when it’s due, as your credit card interest is likely to be higher than your home loan interest. Carefully managing your spending is also key, so consider whether this approach is right for you before signing up for a credit card.