Superannuation is a long-term investment designed to help Australians save for their retirement. For many retirees, superannuation is increasingly providing a large part of their retirement income. That’s why it’s important to consider how your superannuation is invested. The decisions you make about how your superannuation is invested today can have a significant impact on your retirement.

In this article, we’ll explore the risks of leaving your superannuation in cash, the importance of diversification and how taking an active role in managing your superannuation can improve your outcomes in retirement.

The risks of leaving your superannuation in cash

If you’re a member of the Macquarie Superannuation Plan (the Fund), your superannuation or pension account includes a central cash flow account (cash account). The cash account is like a bank account that’s used in the day-to-day administration of your superannuation or pension account. All regular transactions into or out of your account, including superannuation contributions, taxes, pension payments, fees and charges are processed through the cash account.

Given the transactional nature of the cash account, leaving all, or a large portion of, your superannuation in this account for the long term carries some risks:

- Inflation impact: Inflation refers to the gradual increase in the prices of goods and services, which reduces the purchasing power of money over time. For example, $100 today will likely buy less in the future due to inflation. While the cash account pays interest, the rate of return is typically lower than other investment options and is unlikely to outpace inflation consistently. This means that even if your balance appears to grow, its value - what it can actually buy - will decline over time.

For information on the current interest rates applicable to the cash account, visit the Product information page on our website. - Longevity risk: Longevity risk refers to the possibility of outliving your retirement savings. With life expectancies increasing, many Australians are spending 20 years or more in retirement. If your superannuation remains in the cash account and doesn’t achieve sufficient growth, your savings may not last throughout your retirement.

For information on some of the key risks to be aware of when investing your superannuation, read our article Managing risk in retirement.

The importance of diversification

To mitigate these risks, it’s essential to consider a diversified investment strategy that aligns with your financial goals, risk tolerance, and retirement timeline. Diversification involves spreading your investments across different asset classes - such as shares, property, fixed income, and cash - based on your specific needs and circumstances.

Each asset class has its own risk and return characteristics. For example, shares and property are typically considered growth assets, offering higher potential returns over the long term but with greater volatility. On the other hand, fixed income and cash are defensive assets, providing stability and liquidity but generally lower returns. The investment options you select will depend in part on how comfortable you are with risk.

By allocating your superannuation across a mix of growth and defensive assets, you can balance the need for long-term capital growth with the need for short-term security. This approach can help you to achieve a sustainable retirement income while protecting against risks such as inflation and longevity.

A financial adviser can help you develop an investment strategy that’s tailored to your individual goals, circumstances and risk tolerance. They can also assist in regularly reviewing and adjusting your investment strategy to ensure it remains appropriate, as your circumstances are likely to change over time.

For information on investing your superannuation, read our article on Understanding your superannuation investment choices.

Example

Carla has approximately $400,000 in superannuation. She hasn’t selected any investment options, and her superannuation is currently held in the fund’s cash account.

About Carla:

- Age: 55

- Annual income: $100,000

- Desired retirement age: 65

- Superannuation balance: $400,000

- Interest rate on superannuation cash account: 2.55% (after fees and tax)

- Superannuation guarantee contributions: 12%

Carla heads to the Superannuation Calculator on the ASIC Money Smart website. This calculator can help you work out:

- how much superannuation you'll have when you retire, and

- how investment returns and fees affect your superannuation balance.

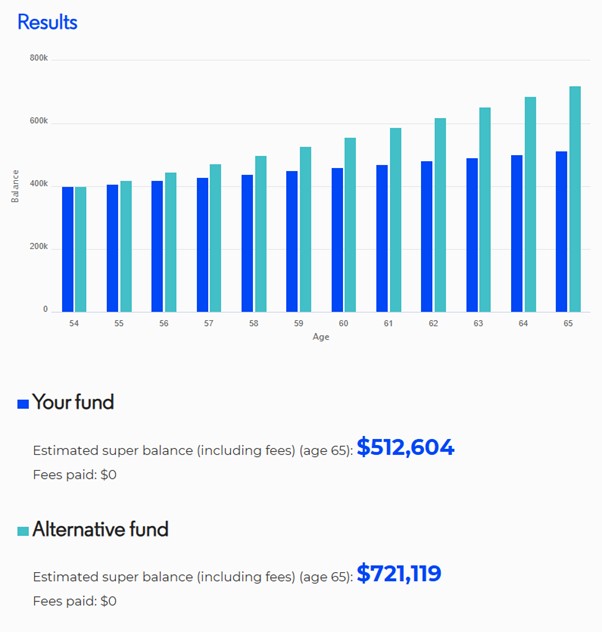

The calculator shows that, if Carla continues to hold her superannuation in the cash account, her balance is projected to be around $512,604 by age 65 (scenario 1).

The impact of investing

Carla speaks to a financial adviser, who recommends she move her superannuation from the cash account into a balanced investment option, which has an average long-term return of 6.2% per annum (after fees and tax).

The calculator shows that, if Carla switches investment options as recommended by her adviser, her balance is estimated to be $721,119 by age 65 (scenario 2). This gives her around $208,515 more in superannuation at retirement than under scenario 1.

The chart below, taken from ASIC’s Superannuation Calculator, illustrates the difference in Carla’s superannuation balance.

The above calculations are expressed in today’s dollars, using an annual inflation rate of 2.5%. The investment option in scenario 2 is based on the ASIC Superannuation Calculator’s default assumptions for a balanced investment option. The calculation was done on 11 September 2025. All other assumptions are detailed on the calculator’s website. If you’re using the calculator with a specific investment option in mind, you may wish to change the default assumptions to reflect the investment’s returns, tax and fees.

Taking control of your superannuation

Superannuation is one of the most important tools Australians have to save for their retirement.

Taking an active role in managing your superannuation may help you achieve a better position in retirement. Whether you’re just starting your superannuation journey or nearing retirement, seeking professional advice from a financial adviser can help you make informed decisions about how your superannuation is invested.